Scholar mortgage debtors received a one-two punch of unhealthy information to bookend the month of June.

Initially of the month, debt ceiling negotiations nixed additional pupil mortgage fee moratoriums. Come September, funds resume come hell or excessive water.

Then, on the finish of June, the Supreme Courtroom dominated that President Biden’s proposed pupil mortgage forgiveness program exceeded the powers of his workplace.

Many People’ budgets are positive to pressure within the coming months and … nicely, for nonetheless lengthy it takes to repay their loans.

Although, debtors is probably not those with essentially the most to lose.

Sure corporations are positioned to take successful as pupil mortgage funds tighten the pocketbooks of over 43 million People. A mean of $393 every month, per borrower, will primarily be sucked out of the economic system and into debt servicing. (That’s over $20 billion per yr!)

And client discretionary shares — the businesses that make nonessential gadgets — are caught within the crosshairs.

Considering on this, I scanned a number of shares within the Shopper Discretionary Choose Sector SPDR ETF (NYSE: XLY) to see which of them charge poorly on my six-factor mannequin, and thus could also be underneath stress if we see a dramatic contraction in discretionary spending.

If the Supreme Courtroom Justices have funding accounts — enjoyable truth, they’re exempt from the stock-trading guidelines Congress should observe — they’re most likely promoting these names as they tighten the screws on disposable revenue…

The King of Discretionary Spending

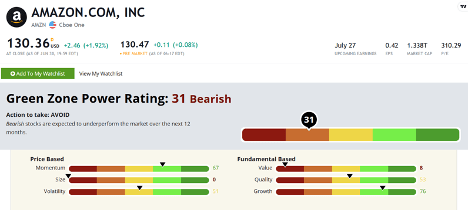

Amazon.com Inc. (Nasdaq: AMZN) could signify the final word discretionary spending firm. And with its behemoth, $1.3-plus trillion market cap, it makes up 23% of XLY.

Not solely is AMZN a just about infinite market for all method of nonessential items, its expensive Prime membership is the gateway to getting all of these items rapidly … and accessing different nonessential companies equivalent to video and music streaming.

Even Amazon’s grocery enterprise, Entire Meals, might take successful as customers search for cheaper important meals choices.

These purchases might be a few of the first that income-restricted prospects look to chop as they make room for pupil mortgage servicing.

Granted, a lot of Amazon’s income comes from its cloud computing service AWS, which is contained from the discretionary facet of issues. Nonetheless, slower retail gross sales will eat into its future potential.

What does my Inexperienced Zone Energy Scores system say about Amazon? Let’s have a look…

(Click on right here to view bigger picture.)

Amazon charges a “Bearish” 31 out of 100, getting particularly poor marks on the Worth issue — with most of its valuation metrics extraordinarily overextended.

As we see it, the inventory is priced for perfection. And traders who’ve been chasing the Large Tech shares throughout the current rally could also be getting over their skis.

Amazon is likely to be the most important inventory on my radar that’s set to endure from the resumption of pupil mortgage repayments, however it’s removed from the one one…

Tens of millions Fewer “Coffees”

Sticking on the theme of discretionary-spending corporations, we have now to have a look at Starbucks Corp. (Nasdaq: SBUX).

The corporate infamously sells espresso and … let’s say “coffee-adjacent” drinks at a value multiples larger than what it will be for those who made it at house.

Hypothetically, if simply half of all pupil mortgage debtors stopped shopping for their $6 extra-grande orange mocha chocka frappa … factor from Starbucks 3 times every week, that’s a $156 million income hit for Starbucks each single month.

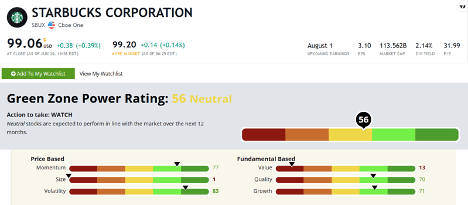

It’s a giant chunk of change. And given SBUX’s already poor Inexperienced Zone Energy Score, additional weak point in income might trigger traders to flee the inventory…

(Click on right here to view bigger picture.)

Starbucks inventory charges a “Impartial” 56 on the Inexperienced Zone Energy Scores system, taking the most important penalty for Measurement and Worth — simply as with Amazon.

This isn’t an terrible ranking, however we are able to’t count on market-beating returns out of it, both. This tells me that Starbucks ought to simply match the market’s efficiency over the following 12 months — up or down.

So there isn’t a lot profit to purchasing Starbucks as an alternative of the S&P 500 … and thus, places you in needlessly larger ranges of danger for that return. By that measure, SBUX is one to keep away from merely for being an inefficient place to maintain your cash.

Although, with regards to the buyer discretionary sector, you can do worse…

My Previous Punching Bag

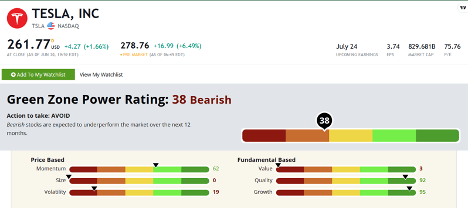

With such a excessive weighing in XLY (19%) … I couldn’t assist however check out my previous favourite punching bag, Tesla Inc. (Nasdaq: TSLA).

Tesla, as a luxurious electrical car maker, is an ideal match for the buyer discretionary class. It does greatest when the economic system is sweet and other people have cash to spend on new toys.

It’s been on an ideal rally in 2023, however does that make it an ideal inventory for the following 12 months? I don’t suppose so…

(Click on right here to view bigger picture.)

TSLA is one other discretionary inventory to keep away from as pupil mortgage funds kick in once more. It charges a “Bearish” 38 out of 100, being a extremely unstable, poor worth and mega-cap inventory.

I’ve spilled quite a lot of ink on these pages and elsewhere on why I feel TSLA is grossly overvalued and susceptible to repricing meaningfully decrease.

Its rally to date in 2023 hasn’t modified a lot for my part. TSLA’s volatility rating alone mainly ensures it is going to fall sooner and additional than the broad market if we get one other downturn.

Talking of one other downturn…

The morning I wrote this, 91% of the shares within the Nasdaq 100 have been down together with the index itself.

That’s not an excellent signal for 2023’s surprise rally, which could simply be stalling earlier than our eyes.

That’s why I just lately got here ahead and revealed a Blacklist of practically 2,000 shares which can be more likely to be money-losers within the months to come back.

Alongside that, I beneficial 11 shares that charge a 95 or above that are set to outperform the market within the subsequent yr. Every one is a high-quality, virtually unheard-of gem that spans all kinds of market sectors.

To get your arms on the tickers on this high-quality, extremely diversified portfolio, get all the main points right here.

To good earnings,

Adam O’Dell

Adam O’Dell

Chief Funding Strategist, Cash & Markets

I discussed yesterday that I’m within the Spanish Basque Nation with my household. It’s pretty, and I like to recommend you place the world in your journey bucket record.

However as I spend time right here, I’m persistently noticing one thing: The service is horrible.

No offense to the waiters, Uber drivers, lodge workers or any variety of different service staff I’ve interacted with. They’ve all been exceptionally pleasant and tolerant of my unintelligible and thickly accented Peruvian- and Mexican-influenced Spanish. They work laborious and put up with rather a lot.

The issue is that there merely aren’t sufficient of them.

After a long time of getting one of many lowest start charges on the earth, Spain has a dearth of younger those that usually deal with service jobs. The explanation it took half an hour for my beer to reach is that the waiter that ought to have been grabbing it was by no means born.

And it’s not simply Spain, after all. It is a drawback throughout the developed world, and it’s at its most excessive within the developed components of East Asia. In South Korea, there have been greater than 40,000 youngster care facilities in 2017. In lower than six years, that determine has dropped to round 30,900, a discount of near 1 / 4.

There usually are not sufficient youngsters to warrant preserving the doorways open.

After all, the opposite facet of that coin is that the inhabitants is ageing. Over the identical interval, the variety of aged services has grown from round 76,000 to almost 90,000.

There are a number of overlapping issues right here:

- How do you assist a nationwide pension or medical health insurance program when there are not any younger folks to contribute, and proportionately, extra of the older generations utilizing the advantages?

- The place does your tax base come from?

- How do you promote your home when there are not any younger households coming down the pipeline to purchase it?

- And maybe most significantly of all, the place do you discover staff?

The brief reply is: “You don’t.”

Sure, immigration may also help plug gaps, however that can also be a zero-sum sport. The brand new immigrant would possibly plug a spot of their host nation, however then that’s one much less employee of their house nation, and the dearth of younger staff is a worldwide subject.

You too can change what you are promoting mannequin. It would sound absurd to go to a bar and pour your individual beer from the faucet, however one thing like that isn’t too far-fetched. Not that way back, bagging your individual groceries or pumping your individual fuel would have sounded absurd.

The one actual resolution is to spice up productiveness or to get extra output from every employee. And synthetic intelligence is a giant a part of that resolution.

I don’t know that AI would have helped a lot in getting my beer to my desk in lower than half-hour. However it’s already enabling corporations to leverage their workforce and change (or scale back) time-consuming and repetitive duties.

And it’s solely simply beginning.

Regards,

Charles SizemoreChief Editor, The Banyan Edge

Charles SizemoreChief Editor, The Banyan Edge

{kind=link}