PixelsEffect/E+ by way of Getty Photos

Park Inns & Resorts Inc. (PK) is undoubtedly one of many greatest model names on the earth. Nevertheless, regardless of its huge title, the actual property funding belief (“REIT”) typically experiences vital drawdowns because of the cyclical nature of its properties.

In in the present day’s evaluation, we enter a dialogue about Park Inns & Resorts to find out whether or not the REIT’s present value presents a profitable entry level.

With out additional delay, let’s get caught into the principle evaluation.

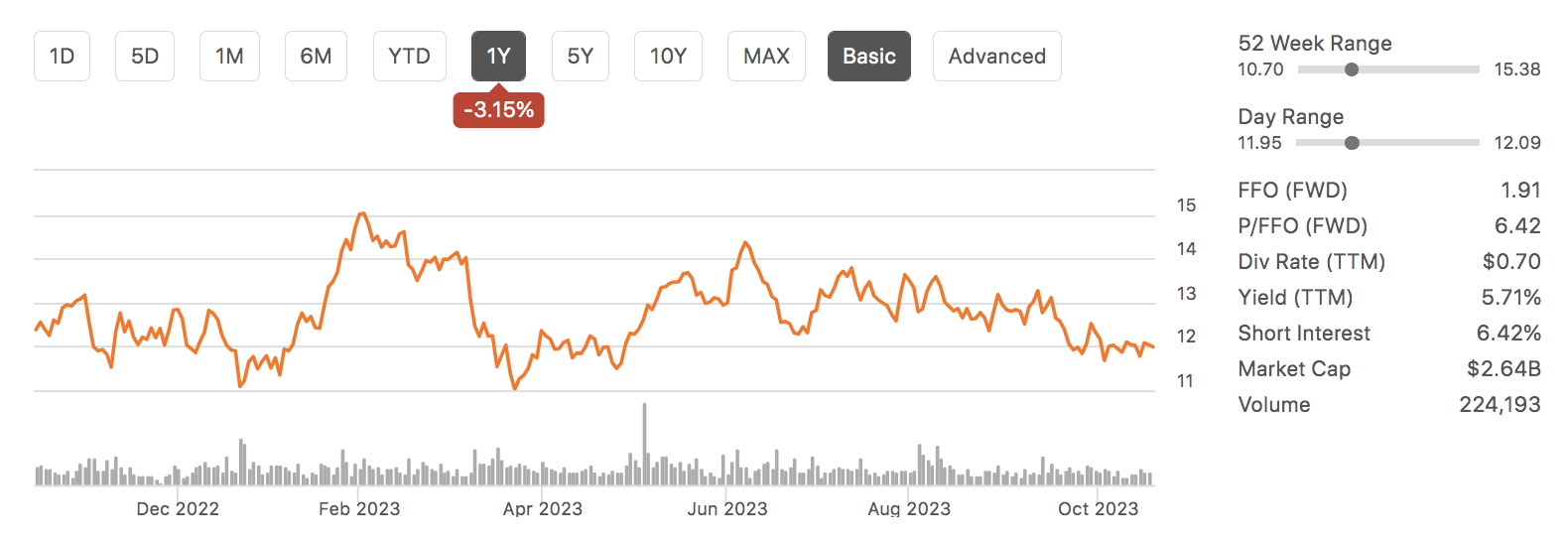

Looking for Alpha

Elementary Evaluation

The Portfolio

Park Inns & Resorts participates within the hospitality enterprise, primarily as a property proprietor, which means it’s ultra-sensitive to cyclical financial swings.

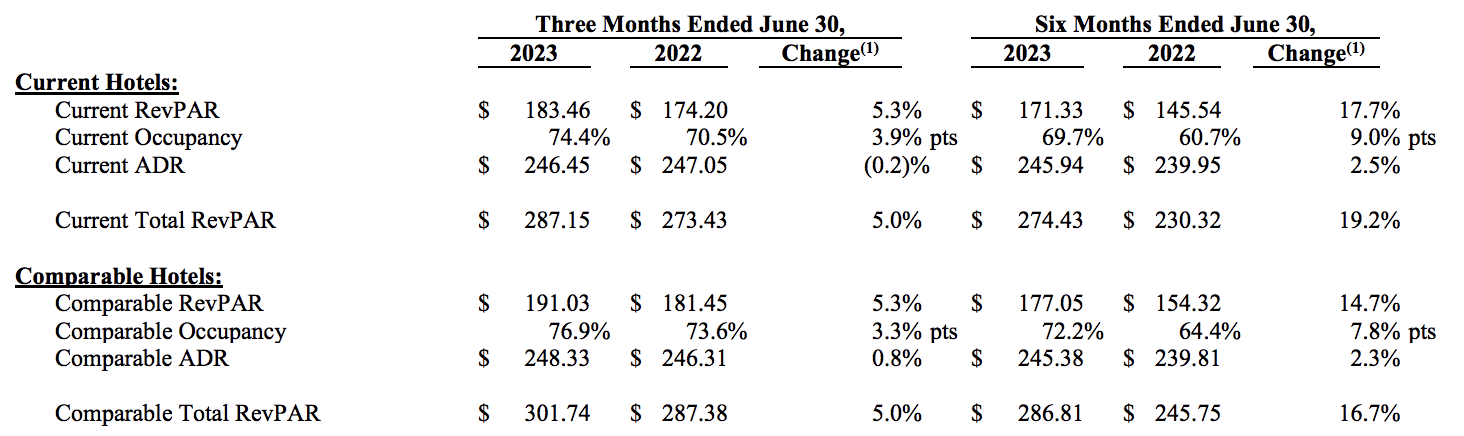

Nevertheless, regardless of the systemic turbulence embedded in in the present day’s actual property market, the REIT is delivering stable outcomes. For instance, Park Inns & Resorts’ second-quarter monetary outcomes confirmed its income per obtainable room is rising sharply with a 5.3% year-over-year improve. Furthermore, occupancy has risen by 3.9% in the identical interval, illustrating growing demand from its shopper base.

Q2 Earnings (Park Inns & Resorts)

Park Inns & Resorts’ present occupancy charge is kind of consistent with the 20-year business common.

It’s typically accepted that increased productiveness/higher-end accommodations expertise much less cyclical habits than lower-end accommodations or motels, phasing out some threat for the REIT’s volatility threat. However, we don’t see occupancy climbing a lot increased than its present degree; 65% can be pushing it.

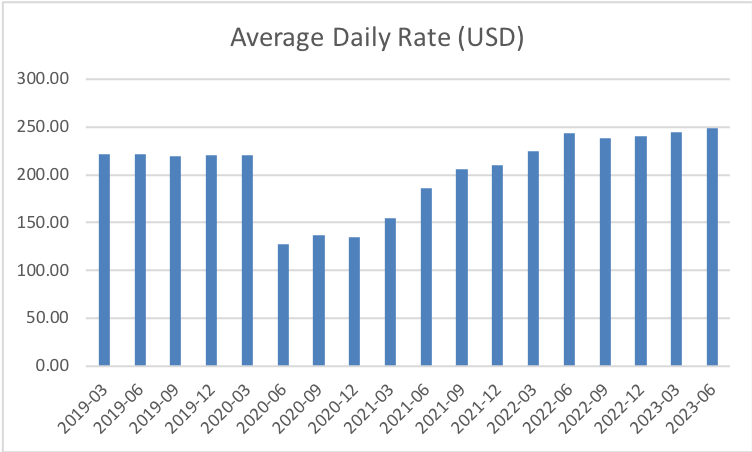

Happily for Park Inns & Resorts, its robust luxurious model permits it to cost excessive costs. Though it’s tapering, inflation stays resilient. Furthermore, individuals are nonetheless on a post-pandemic reopening buzz, presenting Park Resorts and Inns with the scope to cost sustainable costs.

Information from GuruFocus (Writer’s Work)

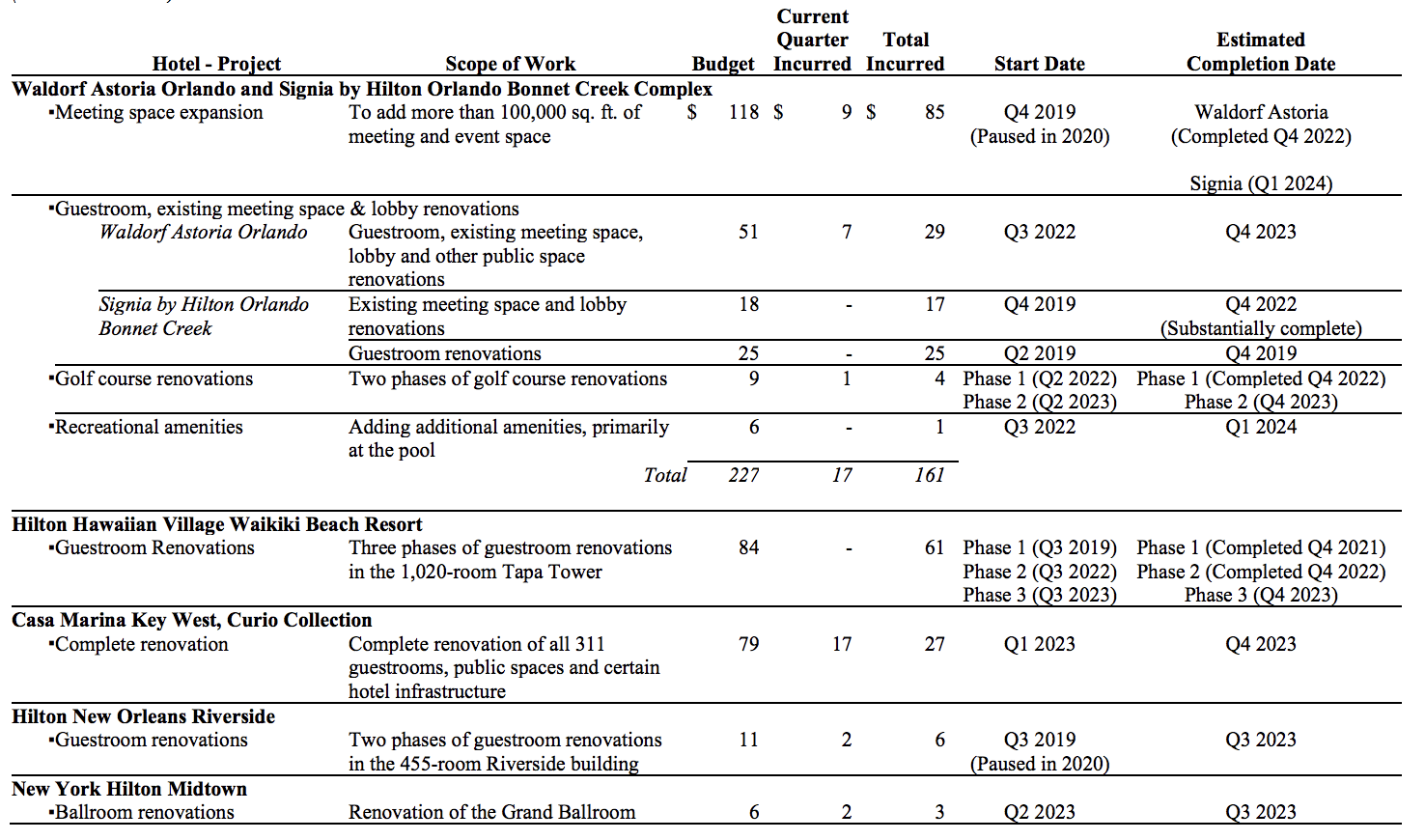

Moreover, the REIT’s CapEx roadmap offers additional latitude for value hikes. As seen within the diagram under, varied renovations and add-ons are occurring, which might all add worth.

The agency plans a full-year spend of $340 to $365 million. We predict exterior acquisitions will begin when debt is extra freely obtainable, however worth will be added by way of inside investments till then.

Growth Pipeline (Park Inns & Resorts)

Lastly, a point out of different revenues.

In our opinion, Meals, Beverage, and Ancillary revenues are contingent on occupancy, which, as beforehand talked about, is scaling. Positive, a touch of elasticity could come into play as shopper sentiment within the U.S. is weakening. However, contemplate that sustainable occupancy and higher-income buyer concentrating on would possibly really stimulate demand.

Park Inns & Resorts

Capital Construction

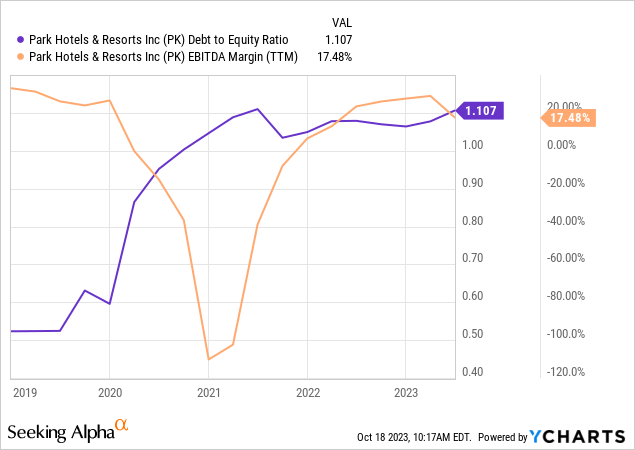

Park Inns & Resorts runs on a debt-to-equity ratio of 1.107 and an EBITDA margin of 17.48%. In tandem, one might say that the REIT is barely overloaded with debt if its reasonable revenue margin is taken into account.

Nevertheless, the online affect in the end is determined by the price of debt.

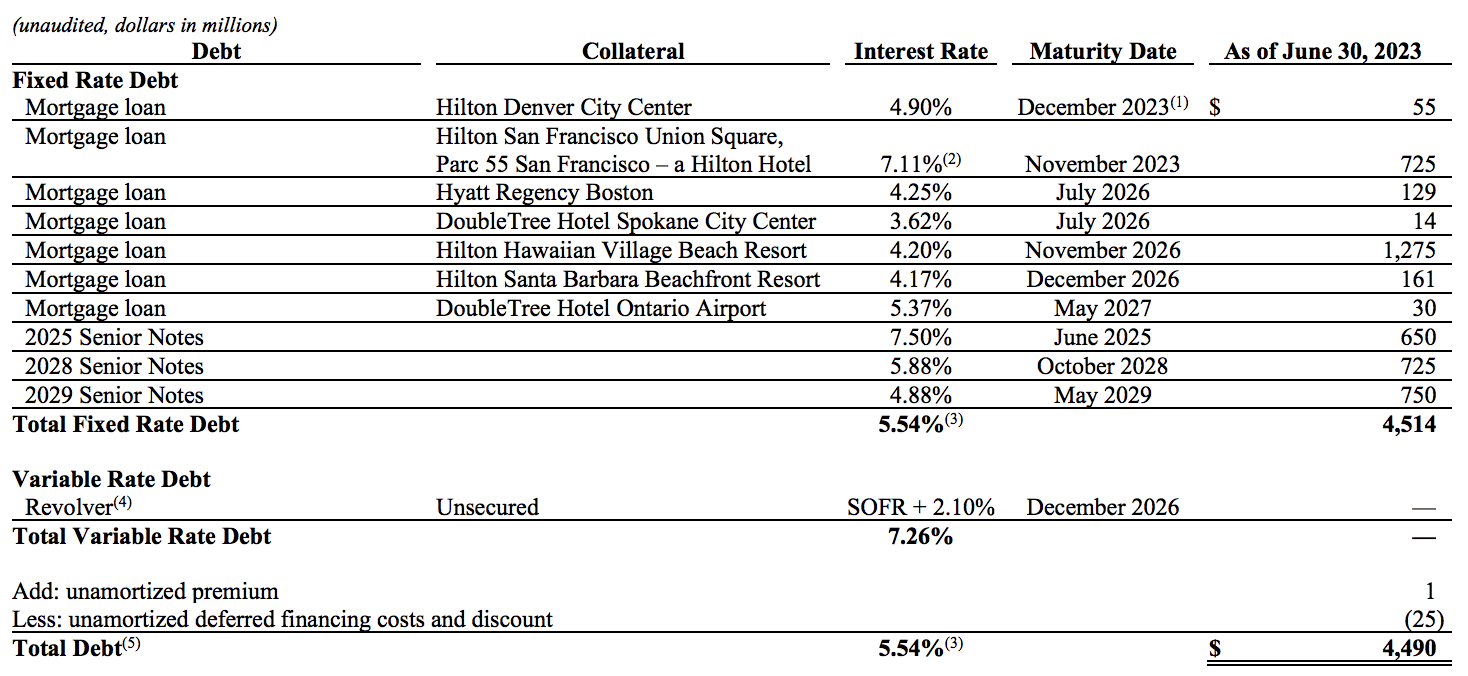

The REIT has a weighted common price of debt of 5.54%. Other than a revolving mortgage, Park’s debt is mounted and holds medium-term durations.

We imagine the REIT’s price of debt is barely increased than what most traders would usually be pleased with. Nevertheless, it should have the chance to refinance at decrease rates of interest when a U.S. charge pivot finally happens, particularly because it possesses a superb credit standing for a hospitality REIT (Final Rated B+ by S&P World).

Park Inns & Resorts

Moreover, the REIT is about to cease funds on a $725 million non-recourse mortgage scheduled to mature in November 2023. Park Inns & Resorts views elements of San Francisco as strategic exits given its underwhelming post-covid restoration. As such, the abandonment of the legal responsibility offers a lot to cheer about because it frees up capital for strategic ventures.

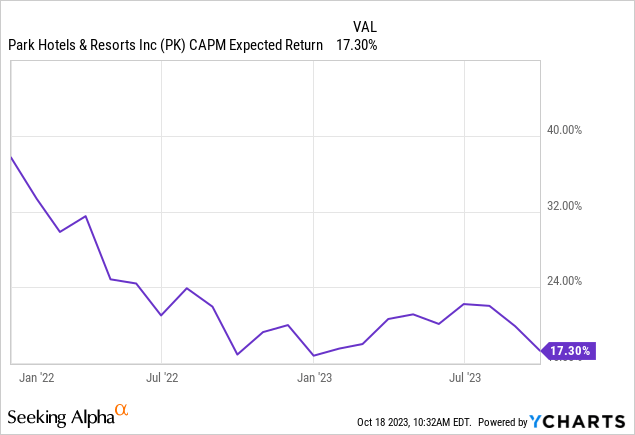

Park Inns & Resorts’ required charge of return threat premium echoes the danger embedded inside its capital construction throughout the earlier phases of the pandemic re-openings. Nevertheless, its CAPM has evidently curtailed since then, implying decrease total threat, which we imagine is essentially on account of higher protection of its credit score obligations.

Valuation

I used the P/E growth method to worth the REIT, whereby I adjusted the components to include the REIT’s funds from operations as an alternative of its price-to-earnings.

In keeping with my findings, the REIT is considerably undervalued, because it possesses a value goal of $22.04. Positive, this valuation method is barely oversimplified and doesn’t assure worth realization. Nevertheless, it’s a useful indicator utilized by many throughout the funding business.

| Variable | Worth |

| FFO Estimated For Dec 2023 | 1.91 |

| Sector Media Ahead P/FFO | 11.54 |

| Worth Goal | $22.04 |

Supply: Information from Looking for Alpha

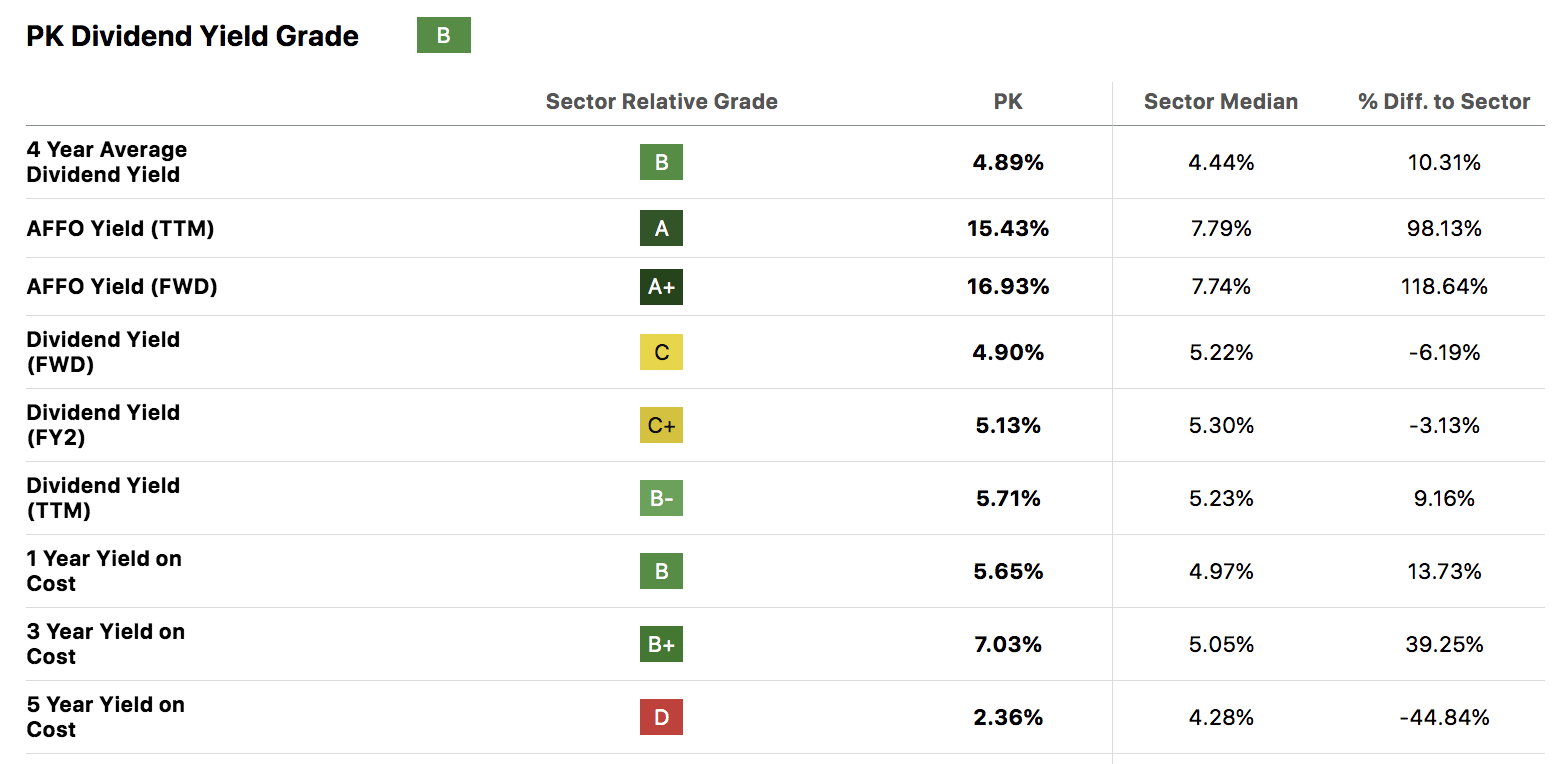

Dividends

At first look, Park Inns & Resorts’ dividend profile appears quite stable. Though cyclicality could come into play, components similar to decrease future rates of interest, a unbroken post-pandemic business restoration, and minimal payout obligations dictate sustainability.

Additional, it’s value contemplating that the REIT offers diversified returns because it operates in a non-traditional sub-sector.

Looking for Alpha

Ultimate Phrase

Our findings mirror that Park Inns & Resorts is gaining momentum and that it’s undervalued.

Particularly, the REIT’s properties are experiencing stable escalation relative to their friends whereas occupancy is above business normal. Furthermore, different income from meals, drinks, and ancillary choices gross sales would possibly correlate with rising occupancy to help broad-based earnings.

Dangers for Park Inns & Resorts Inc. similar to an costly debt profile and cyclical dividends should not be neglected. Nevertheless, our normal feeling is that this REIT is undervalued.

Consensus: Purchase Score Assigned.

{kind=link}