zxvisual/iStock through Getty Pictures

Pricey Buddies and Traders,

The Massif Capital Actual Property technique returned -4.6% internet of charges within the third quarter of 2023, bringing our YTD internet of charges to return to -8.73%.

ATTRIBUTION

|

Portfolio Contribution (Gross of Charges) |

2nd Qrt |

third Qrt |

YTD |

|

Lengthy |

(1.16%) |

(6.92%) |

(4.22%) |

|

Quick |

(0.35%) |

2.70% |

(3.40%) |

|

Gross |

116.27% |

116.20% |

116.20% |

|

Internet |

61.97% |

66.96% |

66.96% |

|

Whole Return |

(1.51%) |

(4.22%) |

(7.62%) |

|

Fairness and Choices E-book (Gross of Charges)* |

|||

|

Vitality |

0.39% |

1.40% |

1.15% |

|

Industrials |

1.11% |

(1.77%) |

0.13% |

|

Supplies |

(3.06%) |

(2.16%) |

(5.52%) |

|

Utilities |

(0.40%) |

(2.07%) |

(3.64%) |

|

Different |

0.45% |

0.38% |

0.25% |

|

Extra Return Information (Gross of Charges)^ |

|||

|

Tail Danger Hedge (Solely Calculated on a YTD Foundation) |

(1.04%) |

||

|

Choices Buying and selling Return |

0.23% |

1.00% |

1.23% |

|

Remoted Return on Dividends Paid |

0.52% |

2.20% |

3.27% |

|

T-Invoice |

0.31% |

0.31% |

1.28% |

|

*Information: NAV, Inclusive of Dividends Paid ^Information: Rolling Estimate based mostly on Massif Calculations |

There isn’t any level in sugarcoating it; the third quarter was abysmal, with a internet of charges return of -4.6%. The lengthy e book sank 6.92% whereas the quick e book rose 2.7%. Losses within the lengthy e book had been pushed by a significant fall within the worth of our Industrial, Materials, and Utilities sectors publicity. The one vivid spot within the quarter was our Vitality sector publicity and the quick e book. This efficiency is less than our requirements, and we make no excuses for that. It’s not the efficiency we would like, it’s not the efficiency our buyers count on, and each effort is being made to enhance efficiency. Sadly, we’ve run right into a nasty buzzsaw primarily pushed by variables exterior our management.

One purpose to speculate with Massif Capital is that we’ve a major focus and experience in industries poorly allotted to by most buyers: vitality, supplies, infrastructure, and heavy business. Inside these sectors, we are likely to carry out nicely on each an absolute and a relative foundation. If we divide our portfolio into Oil and Gasoline, Utilities, Treasured Metals, Industrial/Base Metals, and Industrials and evaluate our returns to the related sector indices, we’ve outperformed three of the 5 this yr.

Sadly, relative efficiency doesn’t spend, however we predict it’s important to spotlight and assess because it helps us perceive the sources of our continued 2023 struggles. The underperformance comes from our metals and mining, the portfolio’s largest allocation, and underperformance in utilities; we’ll focus on each points under. We additionally see a common downward pattern in all 5 of the buckets we put money into.

This pattern prompts us to dig deeper into our returns and assess them from an element stage. Once we decompose gross of charges returns into Alpha and Elements, we discover that issue publicity defined 113% of the drawdown, and alpha was constructive, offsetting the drawdown by 13%. In brief, the businesses we’re invested in proceed to carry out nicely, however our market publicity basically has punished us. With a concentrated portfolio in solely a handful of industries, we’ve to count on that it will occur now and again; it’s not an excuse, only a assertion of reality. Our quick e book is meant to blunt the impression of such occasions, and it did throughout the third quarter, however not sufficiently to maintain efficiency within the black.

Given our in depth evaluate of our quick efficiency this yr, we don’t count on that to alter. Operating a brief e book sufficiently sized to blunt 100% of any drawdowns within the lengthy e book (primarily a market-neutral portfolio) could be very difficult. We proceed to imagine our posture in the direction of opportunistically pushed quick promoting stays the proper plan of action.

SELECT POSITION REVIEW

Utility Publicity (11.8% Gross, 6.3% Internet)

Given rates of interest’ elevated state, it’s maybe unsurprising that our utility publicity has fared poorly for us this yr. We should always have hedged the publicity sooner with a Utility ETF quick, however we didn’t try this till the third quarter, after a lot of the harm was already performed. As famous above, our Utility publicity is second solely to our supplies publicity by way of destructive impression on the portfolio throughout each the third quarter and the YTD durations. That is primarily pushed by our funding in AES, which was down roughly 26% within the third quarter and 47% YTD. Our different utility publicity is up for the yr, together with our quick place, which, as famous, was placed on within the third quarter, and it’s in all probability one thing we must always have had on the books for the complete yr.

We attribute, for proper or flawed, the whole lot of the sell-off in AES to the rate of interest setting. Chart overlays are at all times tough, so one shouldn’t learn an excessive amount of into them, however as a fast sense test of the declare, if one inverts the move-in charges for a generic 10-year US authorities bond and overlay it with AES inventory worth YTD, you get the next:

It’s not arduous to see why we predict rates of interest are the dominant consider AES’s abysmal yr. The worth transfer has pushed the inventory’s dividend yield to five.09% and its P/E to five.2x. The inventory is now buying and selling at a 48% P/E low cost to the imply of its North American Utility Friends (46% low cost to its five-year historic common, a 2.7 StdDev) and a 23% low cost by way of EV/Rev. If the inventory traded at five-year historic a number of ranges, it’s anyplace from a 40% to 80% transfer.

If administration achieves the decrease finish of their adjusted EPS goal (7% to 9% each year via 2025), the corporate will commerce at 4.5x 2025 adjusted EPS. The agency’s five-year monitor report helps modest to robust conviction in administration’s skill to hit their goal. We aren’t dashing to common down, however are including to it slowly over time to take it to six% from its present ~4%. We proceed to imagine the inventory is value one thing within the realm of $30 to $35 per share.

Vitality Publicity (19.7% Gross, 12.2% Internet)

Hydrocarbon investments (oil, pure fuel, LNG, and so on.) is perhaps our most worthwhile investments within the close to time period, because the power of the companies we’re invested in and the favorable medium- to long-term setting continues to favor robust costs in underlying commodities. The superb entry factors we established for our investments had been primarily spurred by a naïve narrative during which oil is perceived to be in a long-term structural decline. We reject this narrative. Whereas short-term economics might negatively impression oil costs, and medium-term provide points are usually accepted, the long-term want for oil is poorly appreciated and poorly understood. Simply as we prompt in a current white paper that there could be no net-zero transition by 2050, there is no such thing as a finish in sight for oil demand. This may increasingly disappoint some individuals and fear others, however it’s a actuality. Absent unforeseeable technological improvements (for instance, sudden breakthroughs in fusion), the world we stay in at the moment, and we suspect for a minimum of the subsequent 50 years, can be powered by hydrocarbons.

Moreover, one doesn’t must tie themselves in knots with advanced evaluation to grasp this straightforward reality. The perfect presentation of the argument was just lately delivered by Arjuun Murti, a former Goldman Sachs fairness analyst on his SubStack Tremendous Spiked.1 The argument begins with recognizing that regardless of the ample funding in renewables, batteries, and numerous vitality options, ongoing demand for oil and pure fuel stays strong and continues to hit new highs.

Most significantly, although, these new highs are being set when no main oil-consuming economic system is in a sturdy financial state. If we hit new all-time highs in day by day consumption throughout a gradual economic system, what’s going to occur in a robust economic system, not to mention a booming economic system?

Taking this line of pondering a step additional, what occurs when elements of the creating world, corresponding to the worldwide south, start to demand extra oil? Will they leapfrog over the hydrocarbon part of the event cycle and transfer on to a post-hydrocarbon world? That’s actually the argument you need to make in the event you count on oil and pure fuel demand to peak by 2030 (because the IEA just lately prompt) and begin to decline. Sadly, that isn’t such a easy argument to make. In any case, oil and pure fuel should not like telephones. A rustic can skip over the landline improvement part and go straight to wi-fi simply. Hydrocarbons (on this case inclusive of coal) presently account for greater than 80% of the first vitality provide globally, and renewables, regardless of their quite a few strengths (and so they do have them), should not the common resolution to energy manufacturing that many declare. Identical to discovering traces of copper in a soil pattern doesn’t imply a copper mine will be constructed the place the soil was taken from, the presence of wind and solar doesn’t imply cost-effective and environment friendly renewables will be constructed. The argument for ongoing demand progress doesn’t finish with strong immediate-term progress.

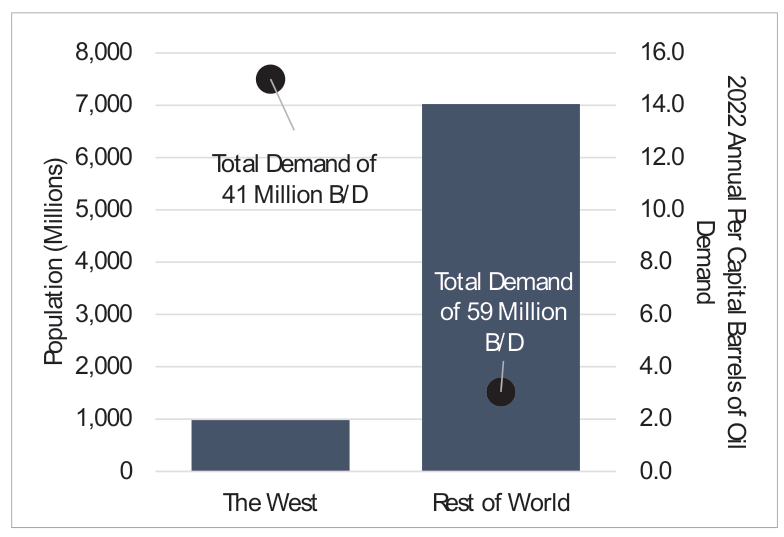

On the present time, with roughly 1 billion individuals, the developed world (US, Canada, EU, Japan, Australia, and New Zealand) has an annual per capita consumption of 15 barrels of oil. The creating world (everybody else) has a inhabitants of roughly 7 billion, with a per capita annual consumption of three barrels. Demand from the developed world has slowed in its progress and should have reversed in locations. With efforts presently underway, it’s even attainable that it’s going to start to say no all through the developed world. Environmentalists are certain to cheer on such an end result, and they need to; there’s nothing inherently flawed with decreasing oil demand.

On the similar time, that developed world pattern doesn’t outline the way forward for oil demand; the longer term can be decided by the 7 billion individuals with rising demand. What occurs if the remainder of the world’s demand doubles, going from 3 barrels of per capita annual consumption to six, which continues to be lower than half of that within the developed world? In that case, day by day world oil demand will increase by roughly 40%. What does day by day oil demand appear like if the worldwide common rises to the usual the West presently enjoys? We attain 334 million barrels of demand a day. We don’t hypothesize that this happens, nor ought to we search it, as it’s unlikely we will meet that stage of demand, therefore the necessity for each vitality supply obtainable (from oil and fuel to renewables and maybe even fusion someday) and our continued help of renewables.

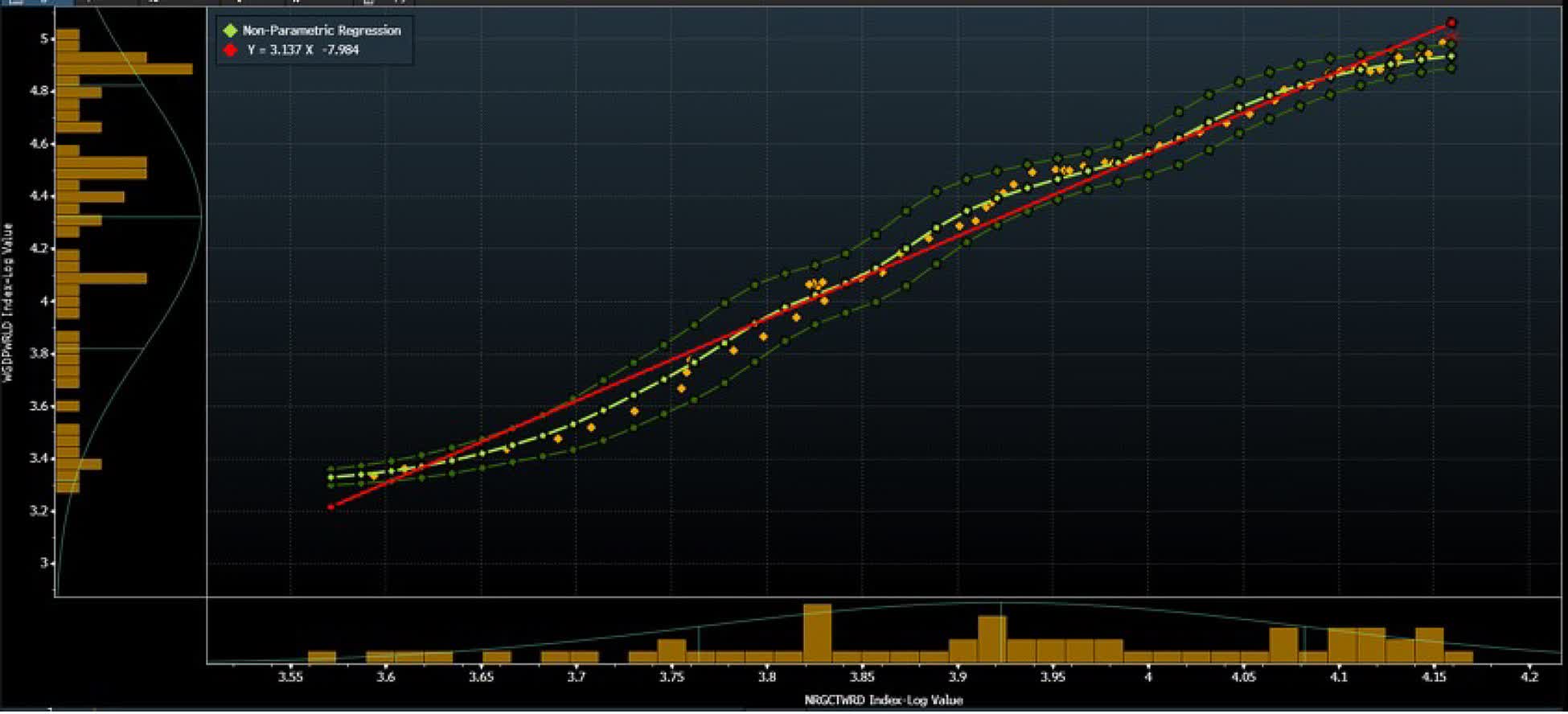

That is the underlying argument for long-term oil and fuel demand. There may be an imbalance in world vitality demand between the developed and creating world that may solely be met with oil and fuel. Moreover, addressing that demand is important for the world economic system and continued efforts at enhancing the lives of seven billion individuals who don’t stay within the developed world. In 2022, 55% of worldwide exajoules of vitality consumed got here from both oil or pure fuel. That quantity doesn’t seize the entire financial impression of oil demand, as 20% of a barrel of oil is used to provide merchandise aside from vitality (chemical substances, plastics, and so on.). Recognizing the important linkages between oil and the remainder of the economic system is crucial as a result of if one regresses world GDP since 1964 in opposition to vitality demand (see chart under), one finds a correlation of 0.98, implying that vitality use and GDP go hand in hand. Prepared entry to vitality instantly contributes to financial progress, which instantly improves the lives of billions.

Numerous advocacy teams, such because the IEA, predict nothing extra aggressive than oil demand stability within the subsequent decade. The IEA World Vitality Outlook 2022 Acknowledged Insurance policies State of affairs (STEPS) suggests world oil demand rebounds and surpasses 2019 ranges by 2023, regardless of excessive costs; it peaks within the mid-2030s at 103 million barrels per day (mb/d) and by 2050 is at 102 million barrels a day. Within the Introduced Pledges State of affairs (APS), extra decisive inexperienced coverage motion brings the height in oil demand to the mid-2020s, with oil demand falling to 93 million barrels by 2030 and 57 million barrels a day by 2050. Within the Internet Zero Emissions by 2050 (NZE) State of affairs, sooner world motion to chop emissions means oil demand won’t ever return to its 2019 stage and can fall to 75 mb/d by 2030.

The Internet Zero State of affairs has already failed as 2019 demand has already been surpassed.

All three situations appear considerably comical, notably the Internet Zero State of affairs. The Internet Zero State of affairs would suggest that within the subsequent seven years, the world will work out tips on how to deal with all incremental vitality demand progress with non-hydrocarbon sources and exchange roughly 14% of the world’s present vitality provide with new non-hydrocarbon-based sources.

The important thing takeaway is that oil and pure fuel costs could also be risky within the quick time period, and demand might decline sometime. Nonetheless, for the foreseeable future, oil and pure fuel provide represents an actual bottleneck to continued financial progress. This could concern everybody no matter your ideas round local weather change, however amusingly sufficient, particularly for local weather change advocates. Any transition to a low-carbon economic system will embody a wholesale remodeling of the worldwide vitality system, the worldwide transportation system, and each provide chain that crosses the globe, therefore our previous suggestion that it’s humanity’s single largest industrial exercise ever undertaken. If you wish to undertake such an exercise, the economic system higher hum; in any other case, we gained’t be capable of afford it.

Given occasions within the Center East on the time of writing, a ultimate notice on geopolitics and oil markets appears warranted. Word that we’re much less interested by making an attempt to foretell the longer term than understanding what everybody else thinks will occur. The long run is unsure, and much more is feasible than we will think about. Nonetheless, the herd’s opinion produces a causal chain of occasions, which is vital to grasp, maybe much more vital than figuring out precisely what’s going to occur, because it lets us consider the dangers embedded in present costs.

The market’s response to occasions within the week of October ninth has shocked us, particularly what we might think about a lackadaisical response to potential threat. As of October 12, oil is up anyplace from 2.8% to three.6%, relying on what you have a look at over the previous 5 days. There was some thrilling motion in oil costs on October 9, however nothing dramatic. It’s tough to not interpret this market response as pricing in a baseline state of affairs the place the present battle doesn’t unfold past Israel’s borders. If the battle stays confined to Israel, world oil provides haven’t any significant menace, therefore a subdued response. We fear that markets should not giving sufficient credit score to a attainable state of affairs during which the present battle spreads past Israel. Ought to that occur, oil costs would spike as provide out of the Center East could be threatened.

The extra important financial impression of such a state of affairs appears poorly appreciated. Trying again to the Seventies, there was a collection of conflicts within the Center East, beginning with the Yom Kippur Conflict in 1973 and adopted by the Iranian Revolution in 1978, that impacted oil costs. Each occasions occurred coincident with the 1973 oil disaster and the 1979 oil disaster. The respective oil shocks that occurred throughout these years had been partly the reason for an enormous stagflationary present that washed over the globe. This isn’t the baseline state of affairs the market is pricing in (nor ought to it essentially achieve this); the market is discounting the prospect of an enormous battle, but it surely stays a real threat that does appear to be ignored.

As occasions in Ukraine demonstrated, the sensitivity of the worldwide economic system to vitality shocks may be very excessive, a actuality we proceed to suppose is oddly underappreciated by the West. Vitality shocks sometimes ship economies into both a dramatic slowdown or a recession mixed with an increase in Inflation, therefore the potential for a stagflationary end result. We might count on central banks to return beneath important strain ought to we see a repeat of oil worth strikes seen within the final two years as they need to select between elevating charges to tame Inflation or chopping charges to spice up progress. Within the Seventies, comparable occasions prompted a de-anchoring of inflationary expectations. Ought to we expertise a variety of battle, it could probably result in the second vitality disaster in two years, an end result we aren’t certain has a historic analog.

Probably the most well-known saying about Inflation comes from Milton Friedman: “Inflation is at all times and in all places a financial phenomenon.” We’re hesitant to boldly (arrogantly) recommend the nice economist makes his case too strongly however discover inflation is extra probably at all times and in all places, a behavioral phenomenon. The potential for shock on the geoeconomic and geopolitical entrance on the present time appears important.

Supplies Publicity (50.8% Gross, 12.7% Internet)

We’re presently considerably chubby Supplies, with a lot of the change from final quarter pushed not by new positions however by a mix of appreciation of our uranium positions and including just a few new shorts to the e book.

Our uranium publicity rallied 67% throughout the quarter, yielding a 1.97% achieve for the portfolio on a place that now represents 8.3% of the portfolio. We’ve got not thought-about trimming but, as we proceed to count on extra worth appreciation from the uranium area. Though we stay solely modestly assured within the claims of a sea change in sentiment round Nuclear, we’re satisfied that even the modest shift that has occurred will be counted on to make sure that the tempo of decommissioning slows (exterior of locations like Germany, which has misplaced its approach with regards to vitality coverage). We additionally suppose that worth stability at present ranges won’t be enough in and of themselves to justify FID on numerous pre-production mines. There isn’t any scuttlebutt to this impact, however we might be shocked to see miners dashing to construct until Uranium shoots the moon from right here or maintains these worth ranges for an prolonged interval. As such, the Uranium provide scenario continues to appear like a coiled spring in our thoughts, with ever larger compression being created due to the straightforward passage of time and steady demand, not to mention modestly rising demand.

Inside Supplies, our investments in Gold (Equinox and an undisclosed junior) and our Nickel funding in Centaurus Metals (CTTZF) are proving notably painful and account for the overwhelming majority of not solely our 2023 losses however our struggles over the past seven quarters. Centaurus alone represents an almost 5% loss for the portfolio on the present time. It is a notably painful inventory to personal as the corporate continues to make first rate progress on creating the Jaguar deposit, together with securing full management of the mines offtake from VALE. However, the distinctive company-level catalysts should not proving enough. The inventory has traded mainly with nickel, which has performed nothing however fall since our funding. The chart under exhibits the normalized return of LME Spot Nickel and CTM since possession; they’ve tracked carefully, aside from a single counter-trend transfer spurred on by a company-level occasion.

We might be mistaken for not acknowledging some missteps in constructing the place, particularly an excessively aggressive entry, which occurred in two methods: First, we took a full 6% place abruptly, slightly than legging into it. We should not have any notes on why we selected to do this, however it’s not our commonplace strategy to constructing a place. Second, we took an aggressive place on the similar time dramatic occasions had been occurring within the Nickel area. As a reminder, there was a pointy quick squeeze within the LME Nickel markets in March/April of 2022; which coincided with the purpose after we completed our analysis and determined to take a place. In hindsight, we must always have let the mud settle earlier than continuing.

Within the wake of the squeeze, Nickel has remained a very tough metallic to consider the way forward for, far more difficult than different metals like lithium or tin which have important progress potential pushed by a mix of conventional expertise and new vitality applied sciences. 4 elements drive the complication on the Nickel entrance:

- The continued emergence of separate pricing, provide, and demand for Class-1 Nickel (the best to transform to Nickel Sulfate for batteries) and Class-2 Nickel (Nickel Pig-Iron, NPI, utilized in chrome steel).

- The oversupply of Class 2 Nickel pushed by a mix of sluggish demand from China, which consumes 70% of the world’s Class 2 Nickel, and surging provide from Indonesia, the world’s largest producer, which, in keeping with knowledge from the Worldwide Nickel Research Group grew output 48% in 2022 and one other 41% in 2023 to date.

- The continued promise of Excessive-Strain Acid Leaching (HPAL) tasks to provide cost-effective Nickel Sulfate within the long-term from decrease high quality lateritic nickel tasks that usually produce Class 2 Nickel.2

- An unclear future for Nickel-heavy lithium-ion battery chemistries.

Relating to the primary difficulty, NPI and Nickel Sulfate costs have already decoupled—from themselves and from LME nickel costs, with NPI presently buying and selling at roughly ~$14,000 per ton in China and Nickel Sulfate at ~$24,924 per ton versus generic LME costs of roughly ~$18,000 per ton. We imagine the discrepancy is because of a number of elements: oversupply of Class 2 Ore, extra strategies to make nickel sulfate, i.e., via conversion of NPI matte/via HPAL, and decrease liquidity in LME Nickel for the reason that 2022 quick squeeze.

We count on continued market fragmentation because the demand for lithium-ion batteries with Nickel-bearing chemistries, corresponding to Nickel Manganese Cobalt (NMC), continues to develop. This fragmentation is sweet for our funding in CTM because the mine, a Sulfide deposit, proposes to promote Nickel Sulfate instantly produced on the mine. This implies they may promote the next value-added product vs. most mines that promote a nickel focus to a refiner (sometimes in China).

Moreover, we count on continued fragmentation of the market, comparable to what’s seen within the oil market based mostly on sulfur content material and weight (API Gravity) however on this case based mostly on CO2 depth. A few of this depends upon how severely automotive producers take efforts to inexperienced provide chains, however the alerts are good, particularly when one is speaking about higher-end EVs promoting into Western markets. Simplistically, we see all metals finally being bought on a Free on Board3 carbon-neutral foundation, that means a premium/low cost could be utilized based mostly on the carbon depth of manufacturing. On this context, Class 1 Nickel and Nickel Sulfate produced from sulfide deposits will earn a premium as a result of inherently decrease carbon depth of the manufacturing course of.

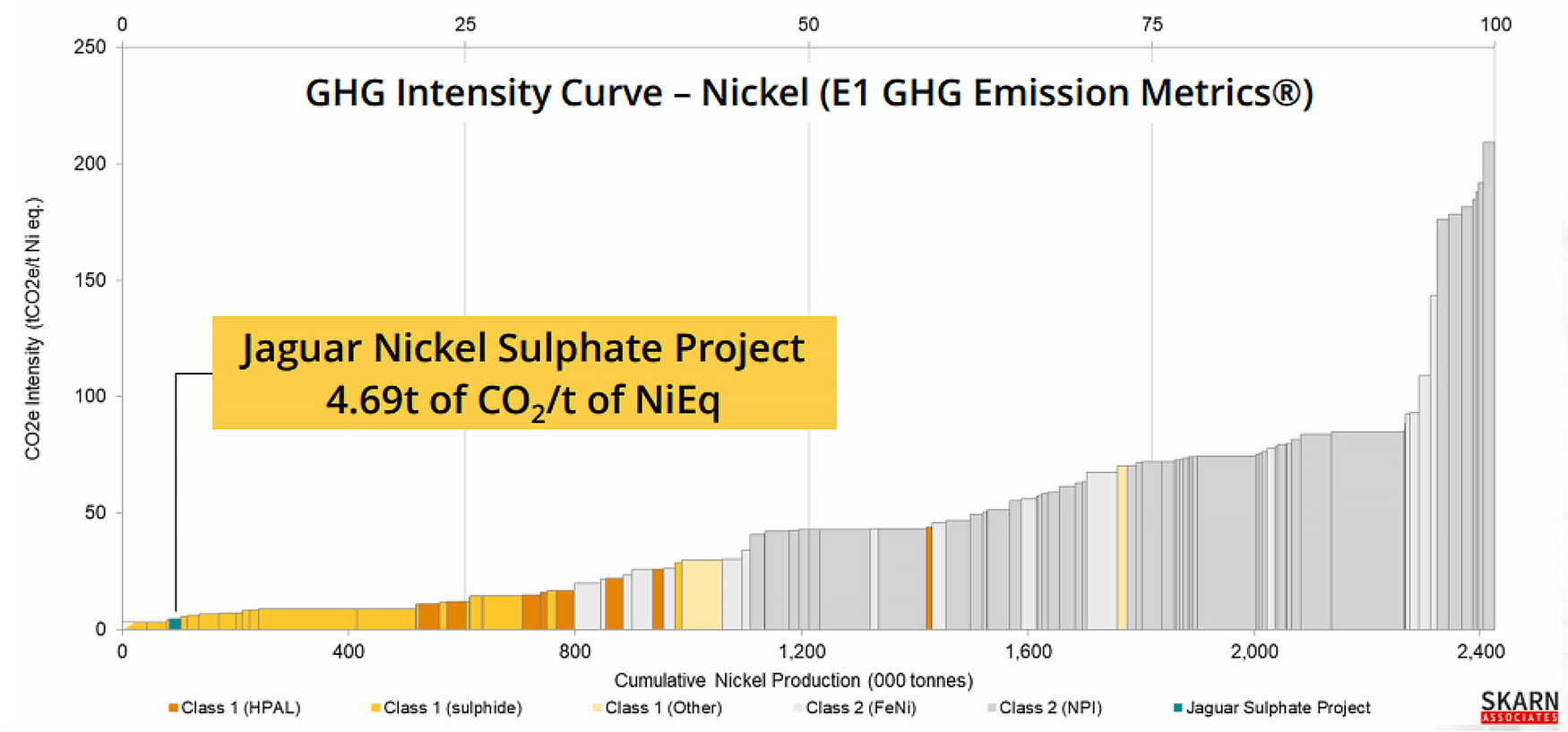

Because the chart of the GHG depth of manufacturing Nickel throughout the business exhibits, the Jaguar deposit has a decrease lifetime of mine CO2 footprint than 97% of worldwide nickel manufacturing. Some might ignore this as simply an amusing factoid concerning the nickel produced by Jaguar, however we disagree. On October 1, the EU formally entered the transitional interval of the Carbon Border Adjustment Mechanism (CBAM)4; the preliminary transitional interval solely requires importers of choose abroad items (together with iron, metal, and aluminum) to report greenhouse fuel emissions embedded of their merchandise.

Within the fullness of time, the EU expects to use the CBAM extra broadly and tax sellers of high-embedded carbon merchandise. This may translate to a aggressive benefit for Jaguar, whose nickel will evaluate favorably with the output of locations like Indonesia, which have low-grade class 2 deposits and make use of energy-intensive processes to transform that nickel into battery-grade nickel sulfate. In Indonesia, the most important world producer of nickel and the supply of a lot of the present oversupply, the path to high-grading poor nickel ore is both by producing nickel matte or by processing the ore through HPAL.

Nickel matte manufacturing is energy-intensive, requiring the ore to be heated to greater than 1,500 levels Celsius, which is completed in a rotary kiln electrical furnace {that a} collocated coal-fired energy plant sometimes powers. HPAL, alternatively, is far much less energy-intensive however produces a nasty poisonous slurry that should be saved in a tailings dam. In both case, the ore from Jaguar is a a lot cleaner product and superior to that which will be sourced from most Asian miners. Admittedly, insurance policies such because the CBAM is not going to save the nickel costs from falling ought to Indonesia ramp manufacturing as a lot because it seems they may, however commodities should not as commoditized as individuals suppose they’re, and low-carbon high-quality nickel sulfate from a western provider will probably earn a premium worth.

Centaurus ought to launch a Definitive Feasibility Research on the Jaguar deposit throughout the fourth quarter, clearing the trail for a ultimate funding resolution someday subsequent yr. This may probably stay a painful funding for a while, however we’ve confidence that the asset’s qualities and the market context will finally yield return.

As at all times, we recognize the belief and confidence you will have proven in Massif Capital by investing with us. We hope that you just and your households keep wholesome over the approaching months. Ought to you will have any questions or issues, please don’t hesitate to succeed in out.

Greatest Regards,

Will Thomson

ENDNOTES 1Tremendous-Spiked | Arjun Murti | Substack DISCLOSURESOpinions expressed herein by Massif Capital, LLC (Massif Capital) should not an funding suggestion and should not meant to be relied upon in funding selections. Massif Capital’s opinions expressed herein deal with solely choose elements of potential funding in securities of the businesses talked about and can’t be an alternative choice to complete funding evaluation. Any evaluation offered herein is proscribed in scope, based mostly on an incomplete set of knowledge, and has limitations to its accuracy. Massif Capital recommends that potential and present buyers conduct thorough funding analysis of their very own, together with an in depth evaluate of the businesses’ regulatory filings, public statements, and rivals. Consulting a professional funding adviser could also be prudent. The data upon which this materials relies and was obtained from sources believed to be dependable however has not been independently verified. Subsequently, Massif Capital can’t assure its accuracy. Any opinions or estimates represent Massif Capital’s finest judgment as of the date of publication and are topic to alter with out discover. Massif Capital explicitly disclaims any legal responsibility that will come up from the usage of this materials; reliance upon info on this publication is on the sole discretion of the reader. Moreover, on no account is that this publication a suggestion to promote or a solicitation to purchase securities or companies mentioned herein. Disclosure: |

Editor’s Word: The abstract bullets for this text had been chosen by Looking for Alpha editors.

Editor’s Word: This text discusses a number of securities that don’t commerce on a significant U.S. change. Please concentrate on the dangers related to these shares.

{kind=link}