Key Factors

- Service Now outcomes level to stable outcomes from different cloud service names.

- Shares like Datadog are overwhelmed down regardless of an expectation for stable progress in 2024.

- Snowflake serves either side of the AI business, offering knowledge administration companies embedded with AI .

- 5 shares we like higher than ServiceNow

Outcomes from ServiceNow NASDAQ: NOW bode properly for cloud companies shares. The corporate posted outcomes that sparked a spherical of surprisingly bullish chatter from analysts that factors to continued energy on this and different cloud companies names.

Analysts considered the ServiceNow outcomes as remarkably sturdy, defying expectations on broad demand, with vital enchancment within the outlook all due to AI. AI is anticipated to and is already proving able to producing substantial price financial savings for companies; it is going to solely acquire momentum and drive enterprise within the cloud. As a result of many of those shares are overwhelmed down on depressed expectations, there’s a vital alternative for them to outperform expectations and reinvigorate their inventory costs.

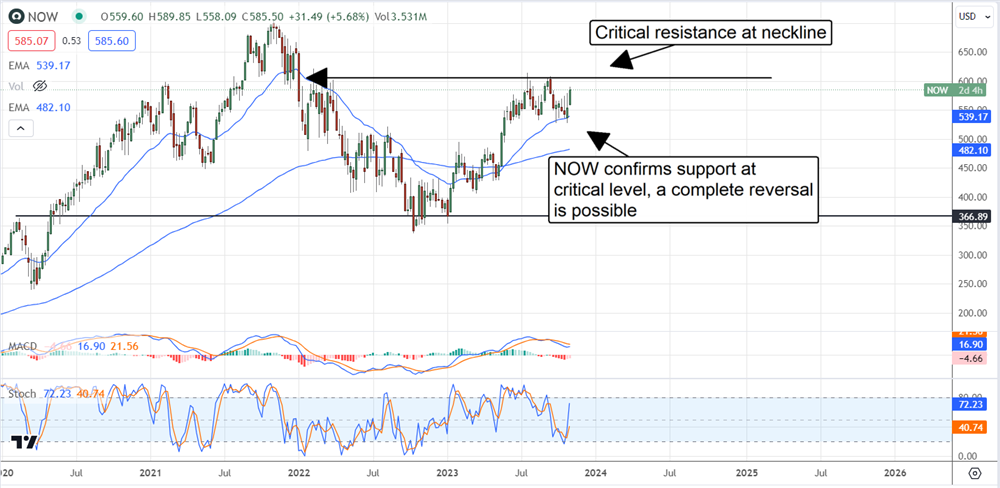

ServiceNow confirms reversal, leads cloud shares larger

ServiceNow had a powerful quarter, with internet revenues up 25% in comparison with final 12 months. The $2.92 billion in income beat consensus by about 100 foundation factors on energy in authorities spending and AI, with income in that section up 75%. Complete subscription income is up 27%, outpacing the consensus by a number of hundred foundation factors, with the remaining efficiency obligation up an equal quantity.

Steerage is what has ServiceNow inventory shifting larger. The corporate raised its steerage for the 12 months, and it might be cautious. A brand new partnership with Deloitte highlights the expansion potential; Deloitte will embed ServiceNow generative AI into its OperateEdge platform, and different giant purchasers are doing likewise. Development of enormous purchasers topped 50% for the quarter, and the penetration is deepening to supply a twin tailwind for progress.

Analysts charge this inventory a Reasonable Purchase and have been elevating their worth targets all 12 months. The Q3 launch sparked one other spherical of revisions, with the consensus goal up 3% in comparison with final quarter and 12% in comparison with final 12 months however in alignment with latest worth motion. The takeaway is that latest worth targets have the inventory buying and selling within the $650 to $700 vary, which is 7% to fifteen% above present motion.

Datadog within the doghouse; market able to rebound

Datadog NASDAQ: DDOG shares sank greater than 20% following the Q2 launch on overreacting to combined information. The Q2 outcomes have been higher than anticipated however got here with combined steerage that included modestly weak top-line expectations however better-than-expected earnings. The takeaway is that income weak point shall be offset by earnings energy, and each targets could also be cautious; Datadog raised steerage considerably in Q1, the Q2 discount is a minor give-back, and outperformance is typical. Concerning subsequent 12 months, analysts venture 25% top-line progress and a wider margin.

The analysts are anticipating good issues in Q3 2023 regardless of the steerage reduce. They’ve solely raised their income and earnings targets for the reason that Q2 launch and have consensus pegged close to the high quality. They’ve additionally been reducing their worth targets for the inventory, placing it on the Most Downgraded inventory record. This exercise has the market buying and selling at a crucial degree and properly positioned for a rebound, given a stable report. Regardless of the downward revisions, analysts see this market advancing greater than 20%.

Snowflake: a blizzard of alternative in AI

Snowflake NASDAQ: SNOW is one other cloud inventory whose share worth is struggling to realize traction regardless of the large alternative in AI. The corporate’s progress slowed in 2023, serving to to cap share worth positive aspects, however an acceleration of enterprise is anticipated subsequent 12 months that may carry vital earnings leverage. The expansion driver for this firm is the necessity for knowledge and knowledge administration, an absolute requirement for creating, coaching, deploying, and using AI.

The corporate is embedding AI companies throughout its platform to assist companies handle and acquire perception from their knowledge. To that finish, Snowflake acquired a number of AI-oriented companies to assist with looking at scale and making use of AI fashions.

Snowflake earnings are anticipated to develop by 50% in 2024, and the bar is probably going low. Analysts have been reducing their targets regardless of persistent high-double-digit progress in giant purchasers and a exceptional 142% internet retention charge. This firm is rising its shopper base and deepening penetration in what many see as the primary innings of the AI revolution, so outperformance is extra doubtless than not. As it’s, income progress is estimated to gradual to twenty-eight% from 35% in Q3 2023.

Earlier than you think about ServiceNow, you may wish to hear this.

MarketBeat retains monitor of Wall Road’s top-rated and finest performing analysis analysts and the shares they suggest to their purchasers every day. MarketBeat has recognized the 5 shares that high analysts are quietly whispering to their purchasers to purchase now earlier than the broader market catches on… and ServiceNow wasn’t on the record.

Whereas ServiceNow at the moment has a “Reasonable Purchase” ranking amongst analysts, top-rated analysts consider these 5 shares are higher buys.

If an organization’s CEO, COO, and CFO have been all promoting shares of their inventory, would you wish to know?

{kind=link}