AnthonyRosenberg

W. P. Carey Inc. (NYSE:WPC) just lately mentioned it would spin off its workplace actual property portfolio and the REIT has lowered its AFFO outlook for 2024 as a consequence.

W.P. Carey just lately up to date its dividend coverage as nicely and plans to pay out 70% to 75% of its professional forma AFFO shifting ahead. W.P. Carey’s up to date dividend coverage and 2024 steerage implies a number one dividend yield of 6.0-6.5% in comparison with a 7.9% yield at this time.

The decrease dividend, nevertheless, nonetheless interprets into a gorgeous yield for passive earnings buyers and WPC is reasonable primarily based on 2024 AFFO.

My Score Historical past

In W. P. Carey: Spin-Off Is A Sport Changer I pointed to the advantages of the belief’s workplace portfolio spinoff. Advantages included a rise within the weighted-average lease price and a de-risked actual property portfolio.

W.P. Carey now introduced its preliminary forecast of 2024 AFFO, following the workplace spinoff, which permits us to calculate an ex-office dividend yield and valuation a number of.

I’ve held W.P. Carey for greater than two years in my passive earnings portfolio and rated WPC constantly favorably, together with when the belief’s inventory traded above $80.

The excessive rate of interest atmosphere has been a headwind for your complete REIT market, together with WPC, which explains not less than to some extent the belief’s poor efficiency.

W.P. Carey’s ad-hoc announcement in September to spin off its workplace properties additionally did some harm to sentiment and created AFFO and dividend uncertainty within the brief time period.

From a dividend protection perspective, nevertheless, I feel that W.P. Carey stays a promising alternative for passive earnings buyers.

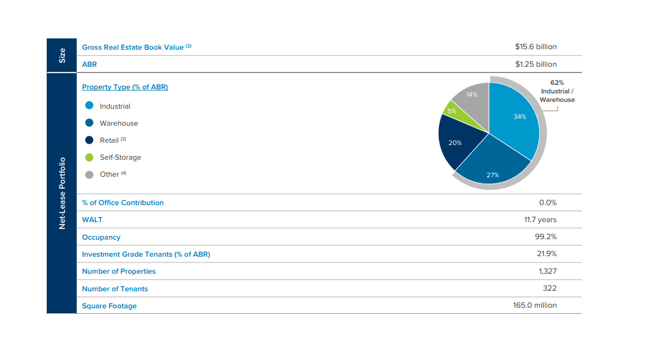

Streamlined Property Portfolio Following Workplace Spinoff

With the exclusion of workplace properties and challenges within the sector, W.P. Carey has rationalized its actual property portfolio. The belief is now extra concentrated in its core enterprise technique industrial and warehouses which collectively account for 62% of W.P. Carey’s annualized base hire.

Although the REIT nonetheless owns a substantial variety of different property in its web lease portfolio, together with retail and self-storage property, I feel the extra refined portfolio positioning makes WPC a much less dangerous funding, notably for passive earnings buyers which can be involved with accumulating secure dividend earnings from the belief’s properties.

Portfolio Overview (W.P. Carey)

The belief has spun off its workplace properties into a brand new entity referred to as Internet Lease Workplace Properties (NLOP) which has begun buying and selling just lately.

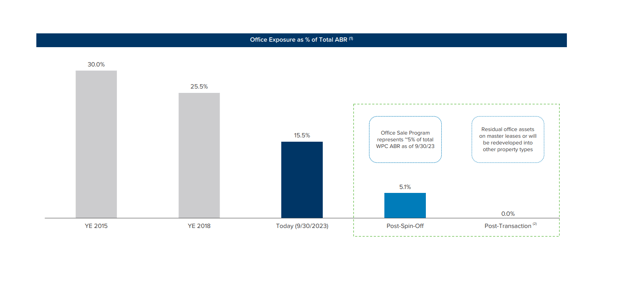

W.P. Carey’s workplace publicity fell to only 15.5% in 3Q-23, down from 30% in 2015, and the elimination of workplace properties, like I mentioned, is a prudent transfer on the a part of administration to maneuver threat off of it stability sheet.

Workplace Publicity (W.P. Carey)

AFFO Outlook for 2023 and 2024, New Introduced AFFO Pay-Out Coverage

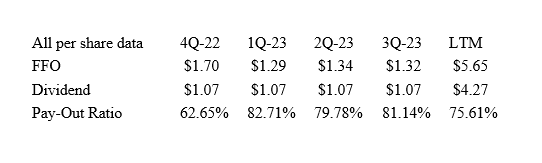

W.P. Carey’s dividend protection within the third quarter appeared pretty much as good as ever. The belief produced $1.32 in FFO whereas paying out $1.071 per share, reflecting an FFO-based pay-out ratio of 81%. Although the pay-out ratio deteriorated 1 share level QoQ, the dividend remained very well-covered.

AFFO (Creator Created Desk Utilizing Belief Info)

Extra attention-grabbing for passive earnings buyers, nevertheless, is the outlook for AFFO and the long run dividend yield that they’ll anticipate as soon as W.P. Carey’s spinoff-related dividend lower goes into impact.

Following the completion of the workplace spin-off, W.P. Carey is seeing AFFO between $5.17 and $5.23 per diluted share in 2023. The belief’s prior steerage referred to as for $5.32 and $5.38 per diluted share in AFFO.

The lowered AFFO steerage implies $1.3 billion and $1.5 billion in acquisitions in comparison with an anticipated funding quantity of $1.75 billion and $2.25 billion previous to that.

With workplace properties now not being a part of W.P. Carey’s core technique, the belief additionally projected a decline in AFFO to $4.60 and $4.80 per diluted share in 2024 which displays a lower of 10% YoY.

Transferring ahead, this vary, $4.60-4.80 per diluted share needs to be the brand new baseline for W.P. Carey by way of FFO and I’d anticipate low single digit progress in AFFO within the years after that.

W.P. Carey additionally clarified that its new dividend pay-out coverage implies that the belief can pay out 70% to 75% of its pro-forma AFFO sooner or later. For 2024, this means a dividend pay-out of $3.22 to $3.60 per diluted share which is a reasonably wide selection.

Primarily based on the center of the vary, passive earnings buyers can anticipate $3.29 to $3.53 per diluted share in dividends for 2024. This implies, primarily based on W.P. Carey’s preliminary 2024 AFFO steerage, an funding in WPC is about to yield between 6.1-6.5%.

W.P. Carey Is Nonetheless Low cost

With $5.20 per share in AFFO (center of the vary) anticipated for 2023, W.P. Carey’s inventory is promoting at an AFFO a number of of 10.5x.

Earlier than the spinoff, W.P. Carey was promoting at an AFFO a number of of 12x and the a number of earlier than that was even greater. Primarily based on the preliminary steerage for subsequent yr, $4.60-4.80 per diluted share, the belief’s inventory is promoting at 11.3-11.8x AFFO, so even when considering the workplace spinoff, the belief is promoting at fairly a gorgeous valuation a number of.

Why W.P. Carey Might See A Larger/Decrease Valuation A number of

W.P. Carey’s valuation a number of continues to be depressed, primarily as a result of buyers want extra time to check the ‘new’ W.P. Carey with out its workplace portfolio footprint.

Uncertainty about anticipated AFFO, ex-office, has additionally been a headwind for W.P. Carey’s inventory value, however with the belief now clarifying its AFFO expectations for 2024, I feel that the valuation stays compelling for passive earnings buyers. My earlier feedback concerning the de-risking of W.P. Carey’s portfolio are nonetheless legitimate as nicely.

My Conclusion

W.P. Carey is rising as a REIT with a rationalized portfolio and a core-focus on industrial and warehouse amenities.

The belief simply introduced its expectations for 2024 AFFO, following the spinoff of its workplace property portfolio, and although W.P. Carey is anticipated to see a drop in AFFO, the valuation a number of primarily based on AFFO seems to be engaging to me.

W.P. Carey continues to be set to supply passive earnings buyers a dividend yield of greater than 6% and I feel that the money circulate steerage for 2024 was really not that unhealthy, implying solely a ten% YoY drop in AFFO.

With a risk-reduced actual property portfolio and readability offered by way of AFFO potential, I feel that WFC stays a purchase for passive earnings buyers.

{kind=link}