Nikada

By Lynn Music

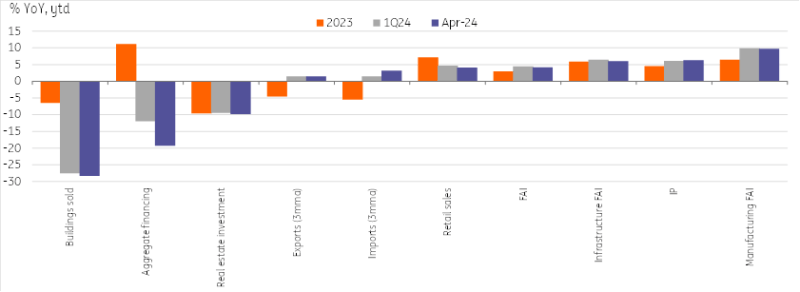

Weak confidence continued to pull progress

China noticed a combined bag when it comes to information releases over the previous month, however most indicators got here in weaker than market forecasts.

The important thing theme for the month was each the non-public sector and households remaining cautious. Credit score information confirmed that mixture financing declined for the primary time since 2005, and M2 progress additionally fell to file lows. After a powerful 2023, credit score contracted sharply in 2024. Our view is that actual rates of interest stay too excessive for the present state of the economic system, and consider there are rising odds for financial easing over the following a number of months.

Retail gross sales confirmed that customers additionally remained cautious, falling to a brand new post-pandemic low of two.3% year-on-year. Shoppers have shied away from big-ticket purchases in favour of the “eat, drink, and play” classes.

Mounted asset funding additionally disenchanted on the month, falling to 4.2% YoY year-to-date largely attributable to a drag from non-public sector funding, which grew a tepid 0.3% YoY YTD. With property costs seeing a pointy decline in April and developer sentiment breaking new lows, it was unsurprising to see that actual property funding remained a serious overhang at -9.8% YoY YTD.

China’s high-tech transition affords a silver lining

A silver lining may very well be the transition towards high-tech improvement, which continues to drive pockets of sturdy progress.

One facet of this transition may very well be seen within the restoration of business exercise. Industrial manufacturing rose to six.7% YoY in April, pushed by high-tech manufacturing (11.3%), computer systems, communications and different digital tools (15.6%) and auto (16.3%). Might’s manufacturing PMI information confirmed conflicting indicators for upcoming momentum, with the official PMI notably falling into contraction at 49.5, whereas the Caixin PMI hit a seven-month excessive of 51.7 – though each surveys indicated a slowdown in new orders.

Imports additionally beat expectations for the month, reaching 8.4% YoY, because of AI-related demand boosting automated information processing tools, built-in circuits, and high-tech product imports. As China’s financial transitions proceed, these areas ought to proceed to see comparatively strong progress.

China’s progress has been unbalanced this yr

CEIC, ING

Coverage rollout has accelerated amid progress stabilisation push

Coverage bulletins stole the thunder from China’s Knowledge Dump Day. Policymakers ramped up supportive measures to attempt to stabilise the property market, and the central authorities kicked off its RMB1tr ultra-long-term bond issuance.

New measures over the previous month included eradicating the ground on mortgage charges, decreasing the downpayment ratios, eradicating buy restrictions, and bulletins of direct housing purchases to assist take up extra inventories. Banks have continued to supply help for ailing property builders.

The elevated aggressiveness of coverage help has supported markets over the previous month and confirmed additional dedication in the direction of progress stabilisation. There was rising optimism in markets that we’ll see housing costs in Tier 1 and a couple of cities backside out within the coming months. Whereas that is arguably a very powerful improvement in stabilising home confidence, it’s also step one and there’s nonetheless extra to be accomplished. July’s Third Plenum assembly will doubtless present additional particulars on the longer-term coverage route, with targets of additional deepening reforms and selling the modernisation of China. Feedback from President Xi indicated that the assembly could embody measures on supporting property, employment, and childcare.

Content material Disclaimer

This publication has been ready by ING solely for info functions no matter a specific consumer’s means, monetary state of affairs or funding goals. The data doesn’t represent funding suggestion, and neither is it funding, authorized or tax recommendation or a suggestion or solicitation to buy or promote any monetary instrument. Learn extra

{kind=link}