The prospect of tighter U.S. restrictions on exports to China and up to date feedback from presidential candidate Donald Trump knocked a few of the wind out of chip shares. Semiconductor shares slid because the Biden administration floated the prospect of more durable commerce restrictions on the business whereas Trump instructed that if elected, he would need Taiwan to pay the U.S. for its protection. Taiwan, house to main foundry operator Taiwan Semiconductor Manufacturing (NYSE: TSM), captures about 62% of the income generated globally by chip foundries, in response to TrendForce. Issues concerning the future led to a sell-off in TSMC in addition to shares like Nvidia (NASDAQ: NVDA) and Superior Micro Gadgets (NASDAQ: AMD), which rely upon TSMC’s fabs for manufacturing and in addition reported vital gross sales to China.

One of many few shares that responded positively to this information from the presidential candidates was Intel (NASDAQ: INTC), whose inventory value spiked sharply greater in Wednesday buying and selling earlier than pulling again for a modest achieve. And whereas that surge of enthusiasm waned rapidly, it was a reminder of why severe semiconductor business traders ought to have a minimum of some Intel inventory of their portfolios.

The state of Intel

Admittedly, Intel’s heyday is probably going lengthy behind it. It lags behind AMD on the chip design aspect of the enterprise, and its new third-party fab operation, Intel Foundry Companies (IFS), is behind TSMC and Samsung by way of course of expertise.

Nonetheless, Intel has the benefit of location: Most of its foundries are exterior of East Asia. Thus, when political figures elevate the prospect of commerce restrictions or say issues that intensify issues that China may invade Taiwan, traders look to Intel as a safer wager.

The supposition that China will invade Taiwan is theory. What will not be speculated is that the chip foundry business is concentrated in Taiwan. To this finish, the U.S. and different Western governments are providing chipmakers tens of billions of {dollars} price of subsidies to construct extra superior fabs within the U.S. and Europe.

Such subsidies profit Intel and its plans to construct state-of-the-art fabs. Moreover, since it’s shopping for essentially the most superior chip-manufacturing gear from ASML, its potential to catch as much as its opponents quickly is healthier than some would possibly assume.

Making sense of Intel’s financials

On account of its investments in constructing out manufacturing capability, Intel’s financials are enhancing, however nonetheless struggling. Within the first quarter, its income rose 9% yr over yr to $13 billion. That was a notable enchancment from its 14% income decline within the full yr of 2023.

Amid heavy investments in its future, it spent 15% extra on working bills. Regardless of that improve, its Q1 web loss shrank to $381 million, a small fraction of the $2.8 billion it misplaced in Q1 2023.

Administration didn’t forecast vital income progress for Q2. Consequently, its inventory has fallen by greater than 30% thus far this yr. Additionally, if there is no political turmoil concerning Taiwan, traders shouldn’t count on the semiconductor inventory to outperform the S&P 500 anytime quickly.

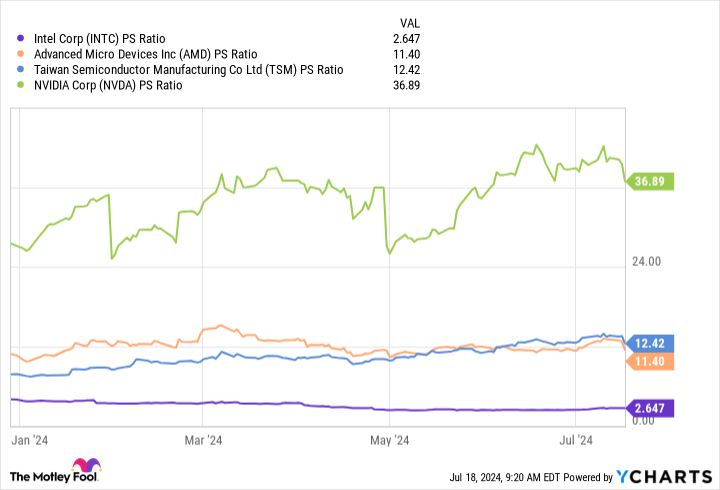

Nonetheless, this inventory trades now at a price-to-sales ratio of lower than 3 — an enormous low cost to its friends.

Nonetheless, the final word measure of Intel’s low valuation is its price-to-book-value ratio of 1.4. This implies its whole market cap is just 40% greater than the market worth of its property. In keeping with the Stern Faculty of Enterprise, the typical book-value a number of within the chip business is above 7, implying Intel inventory is considerably oversold.

Intel as a hedge

Given its present place, Intel is a car traders can use to hedge their positions in chip shares extra intently tied to China and Taiwan, and shares purchased now may ultimately prove to have been a low-cost funding in an business chief.

Admittedly, Intel inventory is unlikely to beat the indexes anytime quickly, and its large investments in itself are not any assure it would catch as much as its friends competitively.

Nonetheless, it’s prone to shut a lot of the hole over time, and its present and future operations within the U.S. and Europe defend the semiconductor business from doable turmoil in East Asia. When one additionally considers its low valuation, an Intel place can defend chip inventory traders and probably produce vital returns in the long run.

Must you make investments $1,000 in Intel proper now?

Before you purchase inventory in Intel, take into account this:

The Motley Idiot Inventory Advisor analyst crew simply recognized what they imagine are the 10 finest shares for traders to purchase now… and Intel wasn’t one in all them. The ten shares that made the reduce may produce monster returns within the coming years.

Contemplate when Nvidia made this listing on April 15, 2005… in the event you invested $1,000 on the time of our advice, you’d have $722,626!*

Inventory Advisor supplies traders with an easy-to-follow blueprint for achievement, together with steerage on constructing a portfolio, common updates from analysts, and two new inventory picks every month. The Inventory Advisor service has greater than quadrupled the return of S&P 500 since 2002*.

*Inventory Advisor returns as of July 15, 2024

Will Healy has positions in Superior Micro Gadgets and Intel. The Motley Idiot has positions in and recommends ASML, Superior Micro Gadgets, Nvidia, and Taiwan Semiconductor Manufacturing. The Motley Idiot recommends Intel and recommends the next choices: lengthy January 2025 $45 calls on Intel and brief August 2024 $35 calls on Intel. The Motley Idiot has a disclosure coverage.

Each Chip Inventory Investor Ought to Maintain a Place in Intel, and We Have been Simply Reminded Why was initially revealed by The Motley Idiot

{kind=link}