You may outline a “low-cost inventory” in some ways, however there’s nothing fairly as basic as a progress inventory altering fingers at a low valuation ratio. With that in thoughts, I extremely suggest taking a more in-depth take a look at freelance companies platform Fiverr (NYSE: FVRR) and memory-chip big Micron Expertise (NASDAQ: MU) proper now. Their shares look deeply undervalued.

Micron: A cyclical upswing

The tech sector runs in broad, sweeping cycles. A market-boosting upswing nearly at all times makes middle-market suppliers too optimistic in regards to the long-term bull marketplace for their wares that could be forming. In lots of circumstances, they wind up left with overstuffed part inventories when excessive demand fades out faster than anticipated. Then everybody will get caught abruptly by the subsequent increase. Demand surges, and the market realizes that the prior bust’s extra provide has all been offered or rendered out of date, and within the meantime, not one of the {hardware} suppliers have constructed any factories since that final cyclical trade downturn began. Then producers should play catch-up to spice up capability in order that they will meet the recent wave of reignited demand.

That is life within the reminiscence chip sector, the place Micron plies its commerce. Proper now, the trade faces hovering product demand as a result of every bit of the bogus intelligence (AI) puzzle requires a ton of high-speed reminiscence chips. Because it occurs, the aftershocks of the coronavirus disaster and flooding disasters in Taiwan left the most important reminiscence makers woefully unprepared to satisfy this surge in demand.

However the upswing is occurring, and I do not see the way it may very well be stopped. From smartphones and PC programs to information heart servers and technology-packed automobiles, the units round us are screaming for extra reminiscence chips. So Micron is ramping up its in-house manufacturing capability with a multibillion-dollar building push in 2025.

Micron’s chip manufacturing and top-line gross sales are trending up after a heavy crunch in 2022 and 2023. Money income and internet earnings are following swimsuit. But it surely’s unprofitable proper now, when it comes to earnings per share. Consequently, Micron inventory may look costly at first look resulting from its detrimental earnings and nonexistent price-to-earnings (P/E) ratio.

However its backside line ought to flip sharply upward over the subsequent couple of years. The inventory is buying and selling at simply 9 instances subsequent yr’s estimated earnings and an inexpensive 4.5 instances gross sales. Lengthy story brief, Micron seems poised to thrive in 2025 and past, and the inventory deserves a richer ahead P/E ratio. It is a stellar purchase at these modest share costs.

Fiverr: Turning a nook on profitability

Many buyers wrote Fiverr off because the beneficiary of a short-lived pattern just a few years in the past. Freelancing gigs in digital trades had been excellent matches for the extreme quantities of free time individuals had through the COVID-19 lockdowns. So Fiverr’s inventory soared to unsustainable heights amid the social-distancing period, then crashed onerous when lots of the platform’s customers and potential customers went again to their workplaces.

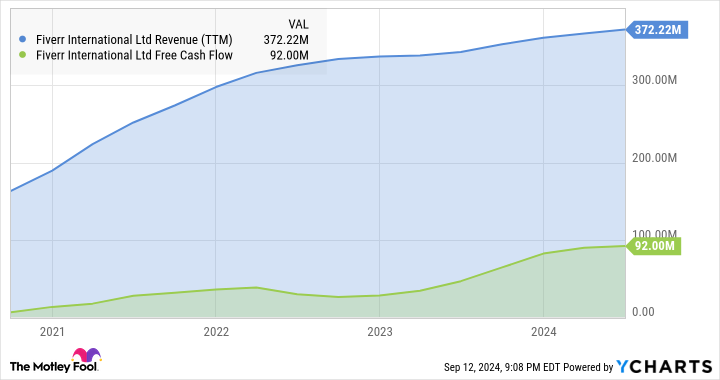

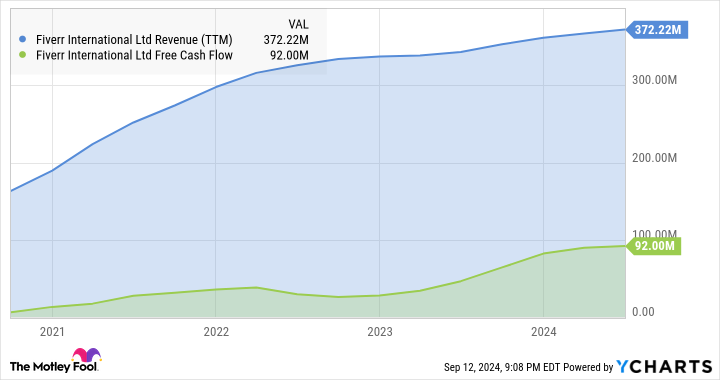

The inventory has been sliding since early 2021, and is down 92% from its peak. However a humorous factor occurred on the way in which to Fiverr’s monetary spoil.

The enterprise by no means stopped rising.

Certain, its after-tax earnings dipped into red-ink territory for some time, and its income progress slowed down from the breakneck tempo of 2020. However Fiverr saved constructing its enterprise, step by undaunted step, whereas pocketing lots of money income alongside the way in which. Fiverr’s gross sales have elevated by 128% in three years whereas its free money flows skyrocketed by 1,400%.

The enterprise is doing simply high-quality, and analysts are beginning to catch on. Backside-line estimates for the subsequent fiscal yr are trending upward and Fiverr’s inventory worth has been struggling to maintain up. Consequently, the inventory trades at simply 9.7 instances estimated ahead earnings and a pair of.3 instances gross sales as we speak.

This little firm has some massive ambitions. In the long term, this gig economic system chief hopes to disrupt the way in which individuals take into consideration careers and work. The corporate has been round for a decade, however remains to be within the early days of a doubtlessly epic long-term progress story. I see an amazing shopping for alternative in Fiverr at its at present modest valuation.

Do you have to make investments $1,000 in Micron Expertise proper now?

Before you purchase inventory in Micron Expertise, think about this:

The Motley Idiot Inventory Advisor analyst workforce simply recognized what they consider are the 10 finest shares for buyers to purchase now… and Micron Expertise wasn’t one in every of them. The ten shares that made the lower might produce monster returns within the coming years.

Contemplate when Nvidia made this listing on April 15, 2005… when you invested $1,000 on the time of our advice, you’d have $729,857!*

Inventory Advisor offers buyers with an easy-to-follow blueprint for achievement, together with steerage on constructing a portfolio, common updates from analysts, and two new inventory picks every month. The Inventory Advisor service has greater than quadrupled the return of S&P 500 since 2002*.

*Inventory Advisor returns as of September 9, 2024

Anders Bylund has positions in Fiverr Worldwide and Micron Expertise. The Motley Idiot has positions in and recommends Fiverr Worldwide. The Motley Idiot has a disclosure coverage.

2 Low-cost Tech Shares to Purchase Proper Now was initially revealed by The Motley Idiot

{kind=link}