Rocket Lab(NASDAQ: RKLB) traders simply carry on successful. The area flight firm is up round 500% within the final 12 months, which is greater than double the returns of Nvidia in that very same timeframe. It has been an unimaginable run for the inventory, led by its growing efficiency in area launches and satellite tv for pc manufacturing, serving to it compete with the dominant participant within the sector: SpaceX.

Here is why traders are uber-optimistic about SpaceX competitor Rocket Lab, and why the inventory is up round 500% within the final yr.

Are You Lacking The Morning Scoop? Get up with Breakfast information in your inbox each market day. Signal Up For Free »

SpaceX has a dominant place in personal business rocket launches. In actual fact, only a few years in the past, the Elon Musk-led firm was nearly the one Western firm capable of reliably launch rockets into orbit. What occurred a couple of years in the past? Rocket Lab started competing for contracts.

So as to enter the market, Rocket Lab focused rocket launches with a lot smaller payloads (i.e., the mass on board) in comparison with SpaceX’s workhorse Falcon 9 rocket. This led it to provide the Electron rocket, which might take small and experimental payloads to orbit. Electron would be the third most launched rocket globally in 2024, which is a formidable feat and reveals how a lot Rocket Lab is making progress to meet up with SpaceX.

Only a few days in the past, Rocket Lab confirmed its true potential with its rocket launch providers, performing two missions (on separate launch pads) in lower than 24 hours. Buyers have gotten enthusiastic about these missions, displaying that Rocket Lab has an opportunity to significantly enhance its launch cadence within the coming years. The demand is there, too. Rocket Lab has a rising backlog value over $1 billion and 1000’s of satellites ready from business clients to be deployed.

Extra launches imply extra income, and finally revenue technology. Since coming into the general public markets in 2021, Rocket Lab’s income has grown 551%, making it one of many fastest-growing companies on this planet. If it may possibly enhance its launch frequency, traders are betting that this progress will proceed for the subsequent few years as properly.

Rocket Lab has bigger ambitions than simply the Electron rocket. By inside investments and acquisitions, the corporate has constructed up capabilities to construct the payloads (satellites, photo voltaic cells, and area pods) for its business clients. Area methods income has grown at a speedy charge in the previous few years and now makes up the vast majority of Rocket Lab’s total income.

The secret’s the flywheel that will get constructed with all these capabilities. Rocket Lab is among the few locations a buyer can go to get a dependable launch into orbit, making it a lot simpler for the corporate to upsell these clients on its area methods capabilities. The federal government thinks it’s a promising enterprise as properly, with Rocket Lab just lately signing a $24 million incentive settlement as a part of the brand new CHIPS Act to construct semiconductors for area methods.

Over the long run, traders ought to watch two developments for Rocket Lab to additional its vertical integration ambitions. First is the bigger Neutron Rocket, which is able to enhance its payload per launch and assist straight compete with SpaceX. The corporate already has a buyer signed on for a Neutron launch, which is anticipated to debut in 2025.

Second, the corporate is planning to construct its personal satellite tv for pc constellation and promote software program/providers from orbit, which may assist increase the corporate’s revenue potential.

There’s a lot to love about Rocket Lab’s enterprise, and I applaud the shareholders who purchased the inventory over a yr in the past. You’re sitting on some incredible good points for the time being. That does not make the inventory a purchase at this time, although.

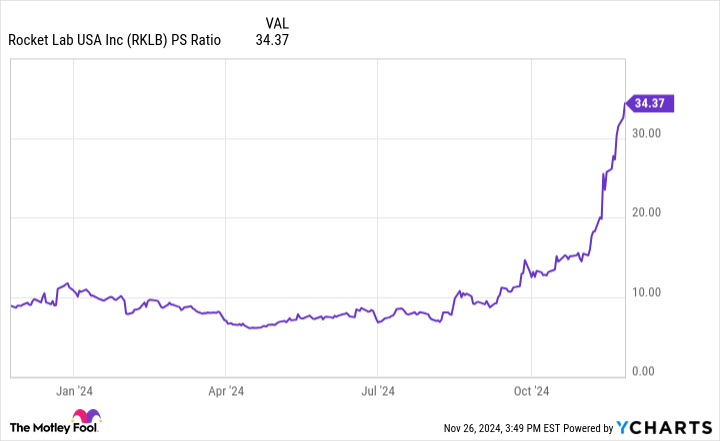

At a market cap pushing by way of $12 billion, Rocket Lab trades at a price-to-sales ratio (P/S) of 34, greater than 10x the market common. Sure, Rocket Lab has a whole lot of progress potential, however this can be a capital-intensive low-margin enterprise that doesn’t need to commerce at over 30x gross sales.

For example this level, let’s carry out some forward-looking estimates for Rocket Lab. In 10 years, if the corporate achieves all of its ambitions with minimal hiccups (an optimistic state of affairs), I may see the corporate’s income rising from its present annual determine of $364 million to $5 billion. With a 26% gross revenue margin, it’s cheap to imagine Rocket Lab can hit 10% internet earnings margins as soon as it scales, or $500 million in earnings on $5 billion in income.

Think about that $500 million in earnings versus the present market cap of $12.34 billion is a price-to-earnings ratio (P/E) of 25. That isn’t a lot decrease than the common S&P 500 P/E ratio at this time, and that may be Rocket Lab’s earnings energy in 10 years below probably the most optimistic assumptions.

Steer clear of Rocket Lab inventory proper now. The inventory worth is getting uncontrolled.

Ever really feel such as you missed the boat in shopping for probably the most profitable shares? Then you definately’ll wish to hear this.

On uncommon events, our professional workforce of analysts points a “Double Down” inventory advice for firms that they assume are about to pop. If you happen to’re frightened you’ve already missed your probability to take a position, now could be the perfect time to purchase earlier than it’s too late. And the numbers communicate for themselves:

Nvidia:should you invested $1,000 after we doubled down in 2009,you’d have $358,460!*

Apple: should you invested $1,000 after we doubled down in 2008, you’d have $44,946!*

Netflix: should you invested $1,000 after we doubled down in 2004, you’d have $478,249!*

Proper now, we’re issuing “Double Down” alerts for 3 unimaginable firms, and there might not be one other probability like this anytime quickly.

*Inventory Advisor returns as of November 25, 2024

Brett Schafer has no place in any of the shares talked about. The Motley Idiot has positions in and recommends Nvidia. The Motley Idiot recommends Rocket Lab USA. The Motley Idiot has a disclosure coverage.

{kind=link}