Joa_Souza

I’ve written about Ultrapar Participações S.A. (NYSE:UGP) twice within the final 10 months. First, in July, I highlighted why this firm was a Purchase amidst the change in gasoline costs made by Petróleo Brasileiro S.A. – Petrobras (PBR). As of March twenty ninth, traders who acted on that article captured a complete return of 53.5% in comparison with 18.3% for the S&P 500. Then, I wrote my second piece in December and argued that the very best was behind us and sensible traders ought to begin to take earnings from their positions because it was unlikely that market-beating returns had been nonetheless on the horizon. The inventory nonetheless had some room to develop and ultimately peaked at $6.33 earlier than retreating to the $5.72 it’s now, which quantities to a complete return of 10.5% in comparison with 13.7% for the S&P 500.

Now, I am downgrading Ultrapar as soon as extra, this time to a Promote ranking. This doesn’t imply you must quick the inventory, it implies that market-beating returns are, for my part, completely off the desk now. The This autumn outcomes had been the height and I will proof that on this article. Moreover that, the valuation I proposed in my first article has been achieved and there aren’t any apparent catalysts to propel the inventory additional. Lastly, for my part, Ultrapar has introduced some questionable M&A recently, as it could elevate some questions by way of how aligned it’s to its present portfolio.

This autumn at a Look

It could be telling that Ultrapar inventory peaked so near its This autumn earnings launch, which was the very best in a number of years. The share value peaked on February twenty third and the earnings name was on February twenty eighth. The corporate was in a position to report vital enchancment in EBITDA, Internet Earnings, Money Stream from Operations, and Leverage, primarily pushed by Ipiranga which accounts for greater than 90% of its income.

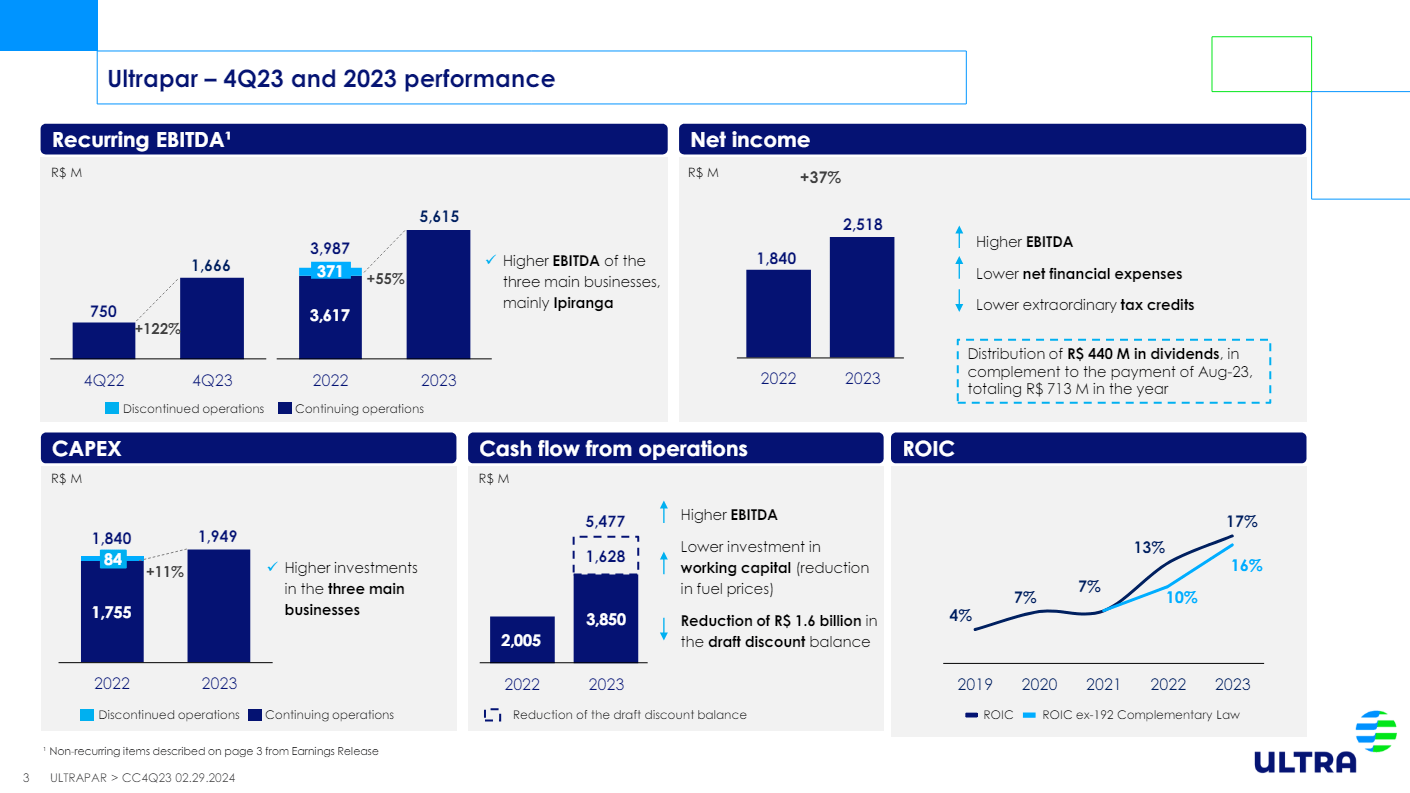

Ultrapar – 4Q23 and 2023 Financials Efficiency (Ultrapar IR)

As may be seen within the slide above, all metrics appear to be optimistic and will have supported the inventory value to go up. Nevertheless, after a run of virtually 200% because the starting of 2023, it is extra possible that each one of these positive factors had been already priced within the inventory and these numbers had been no shock to the market. Primarily as a result of the advance has occurred within the second half of 2023 which may be partially noticed within the This autumn earnings: This autumn’23 EBITDA was BRL 1 billion above This autumn’22 and complete FY’23 was above FY’22 by BRL 1.6 billion.

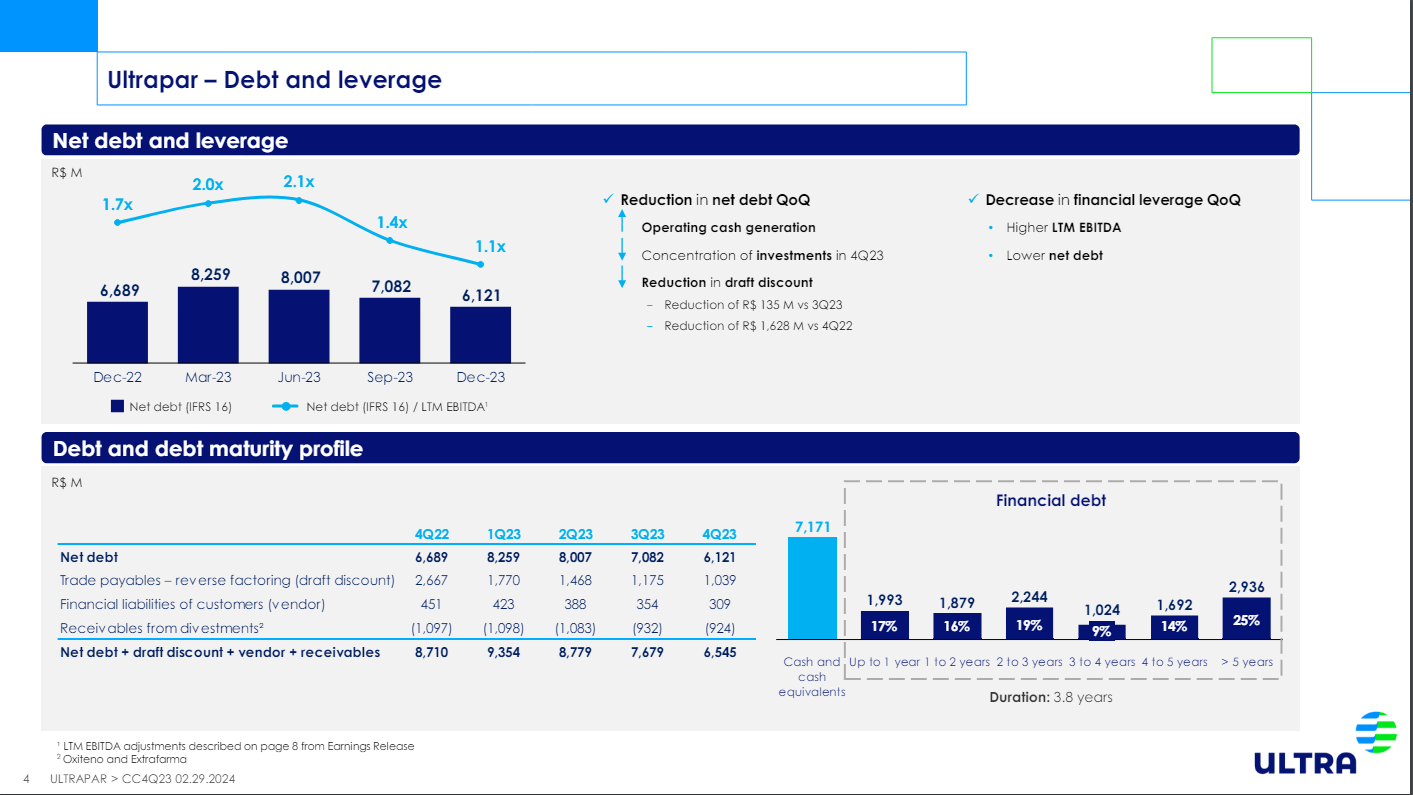

Ultrapar – Debt and Leverage (Ultrapar IR)

One other essential enchancment is the continuing deleveraging course of. Internet debt peaked in FY’21 at BRL 11.8 billion and is now right down to BRL 6.1 billion with Internet Debt / EBITDA at 1.1x versus 3.2x in FY’21. Its Money and Money Equivalents are greater than sufficient to cowl short-term debt retirement and may simply help further Capex or M&A.

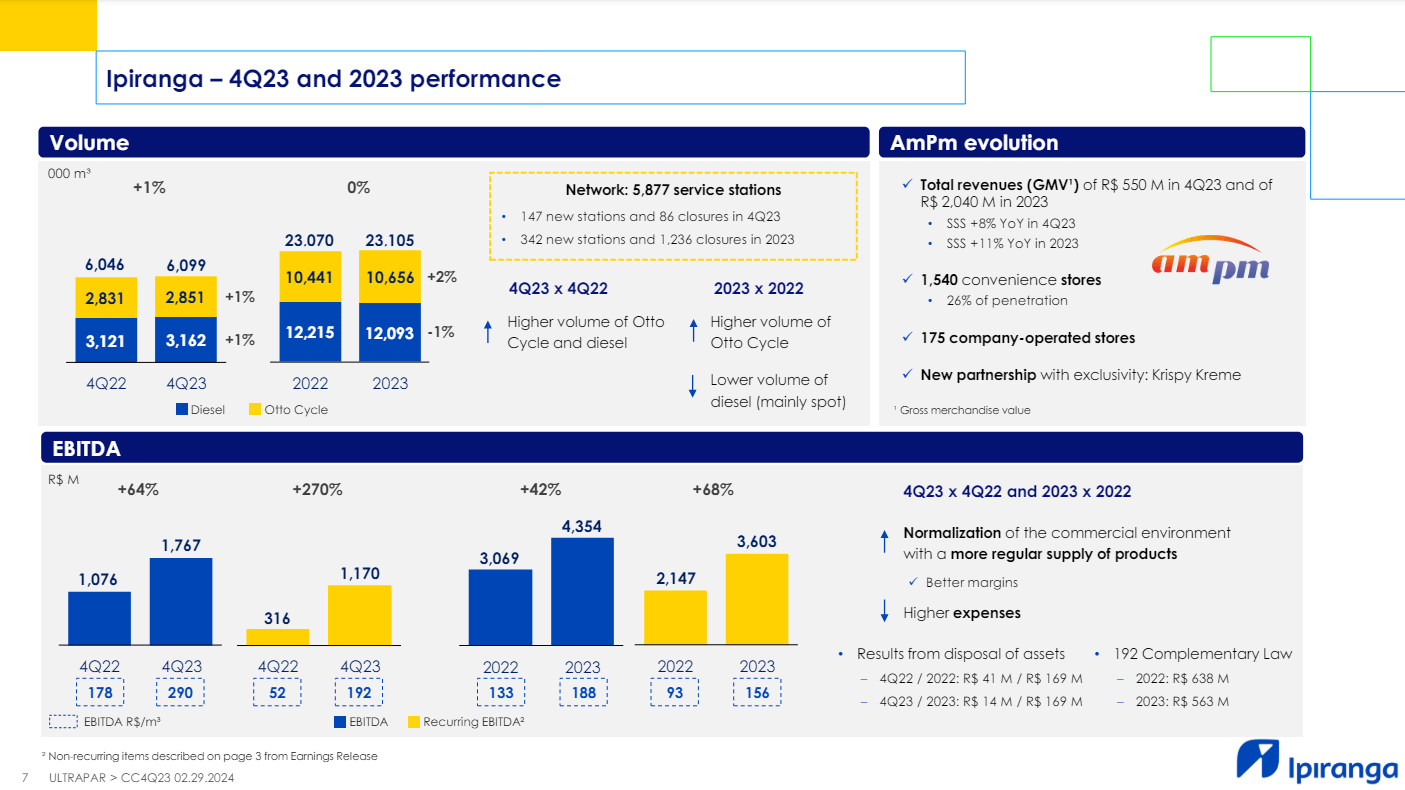

Ipiranga – 4Q23 and 2023 Efficiency (Ultrapar IR)

In my previous article, I praised the developments inside Ultragaz and Ultracargo, however these signify solely 10% of Ultrapar’s income. The primary growth that pushed the refill over the last 12 months is the advance in Ipiranga’s margins. As famous within the slide above, quantity is flat on a YoY foundation, however EBITDA is up +68% if we contemplate the “Recurring EBITDA” measure. That is pushed by Petrobras new value coverage, which, in sum, implies that they will not improve or lower gasoline costs primarily based on worldwide oil costs. A steady gasoline value lowers volatility, makes forecasting a lot simpler, and helps Ultrapar improve margins.

Valuation Test

Within the valuation mannequin I offered in my first article I indicated an affordable value of $5.3 if the result of this gasoline value coverage was optimistic for Ultrapar and a $6.6 value goal if the result was very optimistic. It appears Ultrapar’s gasoline ran out lower than 10% under my $6.6 goal value. I will not element all of the assumptions I used, however the vital expectations had been:

- That Gross Margin had hit rock-bottom in 2022 at 3.5% and that it may climb again to its earlier 2016 excessive of 6.8%. In 2023 Ipiranga managed to report 5.6%, which is a a lot better efficiency than 2022. This autumn was even higher at 7.7% surpassing the previous peak of seven.5% in This autumn’16. Nevertheless, the quarter that adopted This autumn’16 noticed a lower of 1.4p. in Gross Margin. The rationale behind it’s that Petrobras is legally obliged to promote gasoline on the identical value for any gasoline station, be it Ultrapar with virtually six thousand fuel stations or a mom-and-pop fuel station. Each time margins enhance, small homeowners of fuel stations are much less incentivized to be beneath Ultrapar (or some other main model) umbrella and thus imagine it is higher to don’t have any model in any respect, buy gasoline from different intermediaries, and pocket a better margin. That is why I imagine we now have already seen peak Ultrapar efficiency and financials will possible stabilize in FY’24.

- The develerage course of would proceed and achieve success. Certainly, it has been, since Ultrapar has now one in all its lowest ever Internet Debt / EBITDA. Which means that all of the uncertainty associated as to if Ultrapar would be capable of pay its debt and cease bleeding with Curiosity Expense is gone. Additionally, Curiosity Fee has gone down from its peak of 13.75% throughout FY’23 to 10.75%, making Curiosity Bills a lot decrease.

Based mostly on the developments of those two catalysts and the truth that Ultrapar inventory value has misplaced some steam lately, I imagine the height of the cycle is already right here (if not already previous us). I see much less capability for Ultrapar to shock markets with improved financials than I did in early FY23.

Questionable M&A

Lastly, Ultrapar’s M&A monitor report is not the very best one. In 2013 they purchased Extrafarma for BRL 1 billion, solely to promote it in 2021 for BRL 0.7 billion and after incurring losses of BRL 1.5 billion throughout these years. Now, administration has determined that the very best use of the corporate’s money was to purchase a strategic share in Hidrovias do Brasil, an organization that owns and operates ships to move agriculture merchandise in rivers and on the shore of Brazil. The corporate is shopping for a further 17% (they already personal round 10%) for BRL 0.5 billion, to realize a complete of 27% of possession in Hidrovias do Brasil. There could also be some synergy with Ultracargo, nevertheless it’s possible the identical synergy they thought a pharmacy chain had with gasoline stations. Though Hidrovias do Brasil has a long-term debt profile, it is a very leveraged firm with 4.2x Internet Debt / EBITDA and posted a meager BRL 18 million in Internet Earnings for FY’23. It’s at the moment valued at BRL 3.2 billion within the Brazilian Inventory Market.

Extra money may have been used to purchase again inventory throughout FY’23 or possibly pay a particular dividend. It may even have been used to proceed to develop Ultracargo or some other extra correlated enterprise. As an alternative, it was used to purchase 17% of an organization that solely a yr in the past was valued at lower than half what they paid now. Moreover, why would Ultrapar purchase 27% of this firm if not have greater than 50% possession within the close to future? Are they ready for it to extend in worth to purchase it solely?

Last Remarks

In sum, Ultrapar appears to have come full circle. From its unjustified valuation of BRL 10 billion in early FY’23 to greater than BRL 30 billion as of at present. Buyers have virtually no margin of security on this firm and all optimistic monetary efficiency appears to be totally appreciated in its inventory value. As at all times, I may be very fallacious if Ultrapar continues to publish a Gross Margin above 7.0% all through FY’24. That might presumably elevate the inventory increased and generate above-market returns. Nevertheless, I imagine this final result to be not as possible because it was a yr in the past. Buyers would in all probability be higher off exiting their total positions and ready for the following cycle.

{kind=link}