Rick_Jo/iStock through Getty Pictures

After finishing the reverse inventory cut up, Spire World (NYSE:SPIR) shares caught my eye. Analyzing the corporate’s development through the years, each when it comes to monetary efficiency and product, I’ve good causes to imagine that this firm is prime materials for an asymmetrical wager. Notably, the gross margin is extraordinarily excessive, offering a powerful basis for the corporate to turn out to be worthwhile inside the subsequent 2-3 years. Moreover, we’re already nearing vital monetary milestones, with administration displaying their functionality to fulfill the objectives beforehand offered to traders.

With a market capitalization of simply $122 million, the potential upside could be very excessive when one begins to noticeably analyze the outcomes the corporate may produce within the coming years. Moreover, they preserve a strong monetary place, which can additional enhance as the corporate begins to generate money from its core enterprise.

Firm Overview

Spire operates a constellation of nanosatellites. They aren’t optical satellites like these of ICEYE, Maxar, or Capella Area. They’re radio occultation satellites, which use radio waves to check the Earth’s ambiance. This produces knowledge that is distinct from optical satellites, suited to totally different and really sensible use instances.

Spire World gives options helpful for numerous industries:

- Maritime Business – Not solely can ships be tracked when it comes to location, but in addition their traits, their routes, and operations within the ports;

- Climate – Radio occultation satellites excel in learning temperature, humidity, and different atmospheric variables to make climate forecasts. Research performed by the ECMWF, NOAA, and NCAR show that radio occultation know-how can considerably enhance the reliability of climate forecasts;

- Aviation – Spire World’s EURALIO program for the aviation trade gives superior fleet monitoring options and goals to introduce new instruments. For example, the corporate now claims to foretell turbulence and even the power of turbulence;

- Finance – Though the corporate would not expressly focus on it, that is an virtually apparent use case. The huge quantity of local weather knowledge collected from their satellites is actually alpha-as-a-service on the subject of learning agricultural commodities markets.

Whether or not it is aiding an funding financial institution in buying and selling cocoa futures or stopping a cargo ship from falling sufferer to Somali pirates, there isn’t any doubt the corporate gives a helpful product.

Spire’s Vessel Monitoring Instrument – Dwell Demo

SWOT Evaluation

Being a nascent and quickly increasing trade, there are many alternatives but in addition many uncertainties “orbiting” the world of satellites. This uncertainty is clearly an issue solely up to a degree: the place there’s uncertainty, as all the time, there’s potential for market asymmetries.

Alternatives and Strengths

Spire’s primary power is that it is, for now, the one true benchmark for the satellite-to-cloud service tied to radio occultation satellites. There is not any actual competitors for this particular service, permitting Spire to keep up extraordinarily excessive margins. The present gross revenue margin is round 60-65%, and the corporate believes it could possibly attain 70% within the coming years.

One other vital benefit is their capability to defend their aggressive edge by AI and machine studying algorithms that flip satellite tv for pc observations into helpful and accessible knowledge. This implies it would not merely suffice to create the identical satellite tv for pc constellation to supply the identical service.

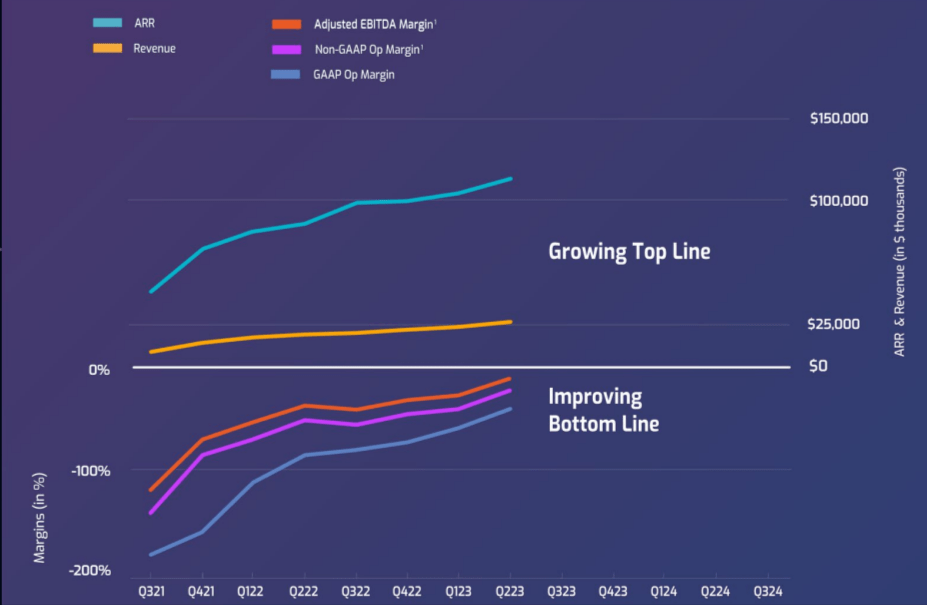

One other important level to emphasise is that the corporate’s enterprise mannequin permits it to generate ARR fairly than spot gross sales. On this, there are two necessary metrics to notice from the newest earnings name:

- The annual retention charge is at the moment over 110%, which means the added worth of current contract expansions exceeds the churn charge worth;

- As of June 30, 2023, the ARR worth was $112.8 million.

Spire World – Q2 2023 Earnings Presentation

Weaknesses and Threats

Greater than weaknesses and threats within the basic sense of those phrases, the principle difficulty for Spire is to make prospects understand the worth of their merchandise and the options the corporate is ready to provide. Knowledge from radio occultation satellites are more durable to interpret in comparison with easy photographs, so not all potential prospects perceive how they may profit from this product.

The corporate lives off an “oblique adoption” course of, at the very least when the shopper isn’t immediately concerned in meteorology. Via APIs, exterior builders can combine the info into their platforms – for instance, ship monitoring knowledge will be built-in right into a broader fleet administration platform.

Thankfully, demo functionalities have been prolonged in current quarters, even stay on Spire’s web site, focusing closely on knowledge processing, not simply assortment. On condition that the final quarter ended with 813 prospects in comparison with 692 final yr, it appears the choice is paying off commercially.

There stays a big unknown represented by the TAM (Complete Addressable Market). Being the one firm that operates this particular service, inside the broader framework of the rising satellite tv for pc huge knowledge sector, it is very troublesome to place a quantity on Spire’s precise potential. Thankfully, the market capitalization is so low that it would not matter whether or not the TAM for knowledge from radio occultation satellites is $5 billion or $15 billion. What issues is that there is loads of room for the corporate to develop, each when it comes to top-line and bottom-line.

Monetary Evaluation

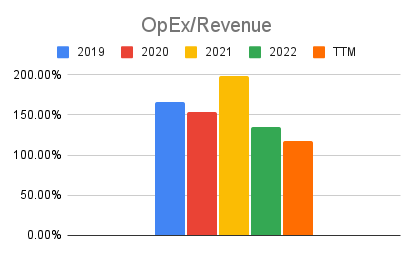

When analyzing Spire World’s financials, it is important to keep in mind that the corporate remains to be extraordinarily younger. Consequently, even when tendencies are rising, we’re nonetheless in a part the place development takes priority over profitability. And contemplating that the corporate goals for a gross revenue margin of 70% with prospects that stay loyal to the service for a number of years, it is a completely logical method.

Earnings Assertion

Under are the actually necessary numbers to concentrate on in the mean time (knowledge in $ million, supply Looking for Alpha):

|

2019 |

2020 |

2021* |

2022 |

TTM |

|

|

Income |

18.5 |

28.5 |

43.4 |

80.3 |

93.5 |

|

COGS |

14.9 |

10.3 |

18.7 |

40.3 |

40.9 |

|

OpEx |

30.7 |

43.6 |

85.9 |

108.5 |

109.7 |

|

EBITDA |

-17 |

-19.9 |

-52.1 |

-50.2 |

-40.2 |

|

Gross revenue margin |

19.46% |

63.86% |

56.91% |

49.81% |

56.26% |

|

OpEx/Income |

165.95% |

152.98% |

197.93% |

135.12% |

117.33% |

|

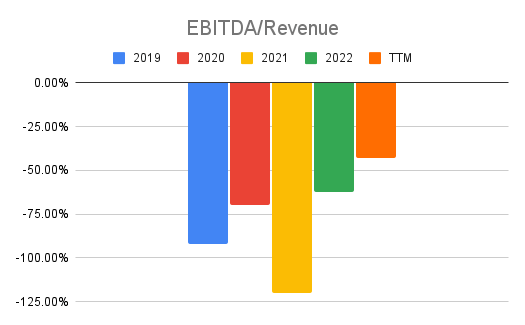

EBITDA/Income |

-91.89% |

-69.82% |

-120.05% |

-62.52% |

-42.99% |

*2021 was marked by merger prices to finish the SPAC

Chart created by the creator – Knowledge Supply: Looking for Alpha

The issues to notice are:

-

The expansion charge stays glorious, even when there is a delay between the contracted annual recurring income and the second when these contracts successfully flip into income. As already talked about, the contracted ARR is at the moment $112.8 million, and the corporate plans to shut the yr at $132 million;

-

OpEx is stabilizing, rising noticeably lower than income in current quarters. The corporate additionally undertook a cost-cutting program to method GAAP EBITDA constructive extra rapidly. The final quarter closed with an OpEx enhance of $0.8 million year-on-year, towards a income enhance of $6.1 million;

-

R&D bills have grown a lot slower than revenues, particularly within the final six quarters.

Chart created by the creator – Knowledge Supply: Looking for Alpha

That stated, it is not possible that the corporate will obtain GAAP EBITDA constructive earlier than 2028. Thankfully, the money movement scenario is significantly better, with Spire anticipating to provide constructive money from working actions as early as subsequent quarter. Furthermore, it goals to turn out to be FCF constructive within the second or third quarter of 2024, which might be exceptionally good for the corporate’s valuation.

Debt and Liquidity

Spire closed Q2 2023 with $97.8 million in present belongings. With solely $40.4 million of present liabilities, of which $21.9 million is unearned income, the corporate has a powerful basis to minimally dilute shareholder possession earlier than turning into FCF constructive. Within the final earnings name, it was highlighted that, cautiously and on days when buying and selling volumes and inventory efficiency are good, among the shares registered final yr are bought to make sure stability of liquidity sources.

On condition that from the tip of 2023, the corporate may also be capable to produce money from its operations, possession dilution should not be a priority. The corporate has nonetheless $130 million in credit score services not in use, and within the final quarter they have been in a position to burn simply $3.7 million with as little as $8.3 million coming from financing. Money burn was a priority, nevertheless it the final couple of quarters we’ve got actually seen the results of the spending evaluate program. With the corporate now much more targeted on profitability, the money burn has been decreased dramatically.

Draw back Threat

The principle dangers related to this evaluation are 4, which I record so as of threat and affect:

- Rivals offering photographs from optical satellites may determine to diversify their operations and enter the radio occultation satellite tv for pc market, rising competitors in an as-yet small market section.

- Spire may not be capable to preserve its development charge over the approaching years, which might jeopardize its capability to realize a constructive GAAP internet earnings. A 25-35% annual development charge, presently, is crucial to make operations worthwhile by 2025-26.

- Even when there are not any direct substitute applied sciences for radio occultation satellites, their utility could possibly be overshadowed by enhancements within the capabilities of optical satellites mixed with AI-based predictive algorithms.

- For now, laws have been favorable to corporations managing satellite tv for pc constellations, however sooner or later, new guidelines may come up necessitating better R&D expenditures and elevated COGS. One instance is feasible anti-debris laws, however that is the least instant threat at current.

Whereas these are current and vital dangers, those with probably the most substantial affect – the entry of recent rivals and the downsizing of the expansion charge – have a low chance of prevalence. No competitor within the optic satellites-as-a-service sector is massive sufficient to think about allocating vital sources to enter the radio occultation satellite tv for pc world, figuring out that the capex can be substantial and that it could take years to generate income. Thus, it is very probably that the market will stay below Spire’s management and that the corporate will be capable to preserve its development charge as a result of absence of true rivals.

Opinions and Closing Conclusions

Spire World is displaying a wonderful development charge, each in revenues and margins. The corporate is within the ultimate levels of utilizing liquidity sources that dilute shareholder possession and is about to begin producing money from its operations. The prospect of reaching a constructive working margin and FCF by the tip of 2024 is one other important issue for my ranking.

There is a strong basis to take a seat tight and let time take its course. With this development charge, these margins, and this retention charge, it is only a matter of time. When it turns into doable to make use of a DCF mannequin to worth the inventory, I imagine Wall Avenue will start to focus significantly on Spire.

No vital catalysts are wanted, only for the corporate to proceed doing what it is already doing. To this point, the corporate has carried out higher than the administration’s steerage, and there isn’t any motive to imagine issues will change sooner or later.

For these taken with small caps with nice potential within the house sector, I additionally suggest studying my evaluation of Terran Orbital: the prospects are similar to Spire’s.

{kind=link}