ryasick

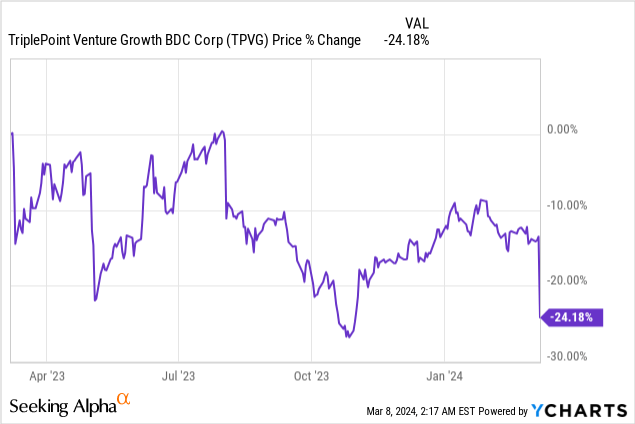

TriplePoint Enterprise Progress (NYSE:TPVG) missed internet funding revenue expectations solely by $0.01 per share for the fourth-quarter, and the BDC’s This autumn ’23 NII was enough to help the $0.40 per share dividend. The BDC’s shares slumped 12%, nonetheless, because the BDC additionally reported a considerable amount of realized funding losses and an 11% drop in its internet asset worth, inflicting new issues concerning the dividend. Because the funding firm reported excessive internet funding revenue relative to its dividend, I consider the market is overreacting to the earnings launch. Nonetheless, I acknowledge that shares have extra danger than shares of different BDCs, like Ares Capital (ARCC).

Earlier Protection

In October, I introduced my preliminary work on the BDC, wherein I mentioned that the dangers with TriplePoint Enterprise Progress had been excessive given the corporate’s above-average non-accrual share. The BDC’s shares had been buying and selling at a near-16% yield on the time, however provided that the non-accrual share has declined since and that TriplePoint Enterprise Progress coated its dividend, I consider a maintain ranking remains to be justified.

A Small, Area of interest BDC Play With Credit score Challenges…

TriplePoint Enterprise Progress is a closed-end BDC with vital investments within the expertise and life science industries. At its core, TPVG has the same funding technique as Hercules Capital (HTGC) which can also be centered on expertise and life science firms that want progress capital. TriplePoint Enterprise Progress invests mainly in debt, but in addition locations “wagers” on sure firms via fairness/warrant investments.

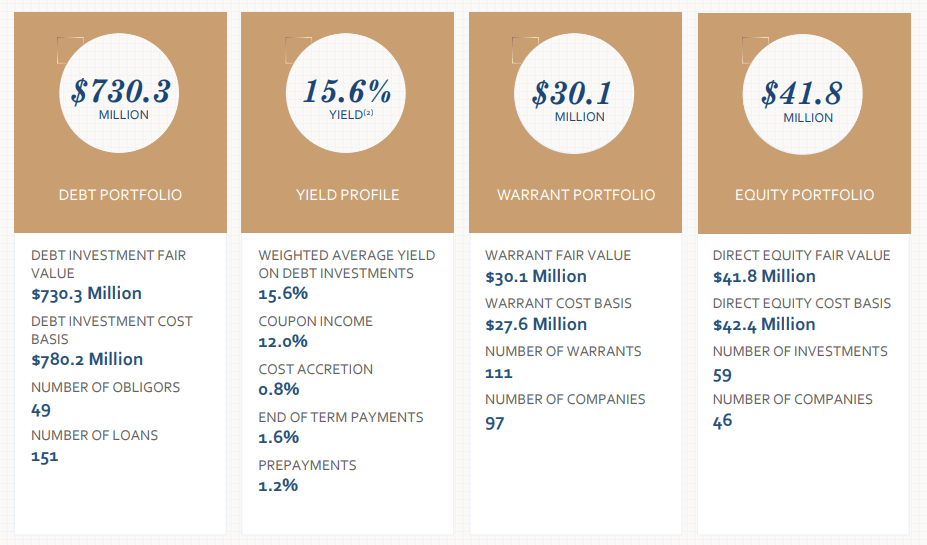

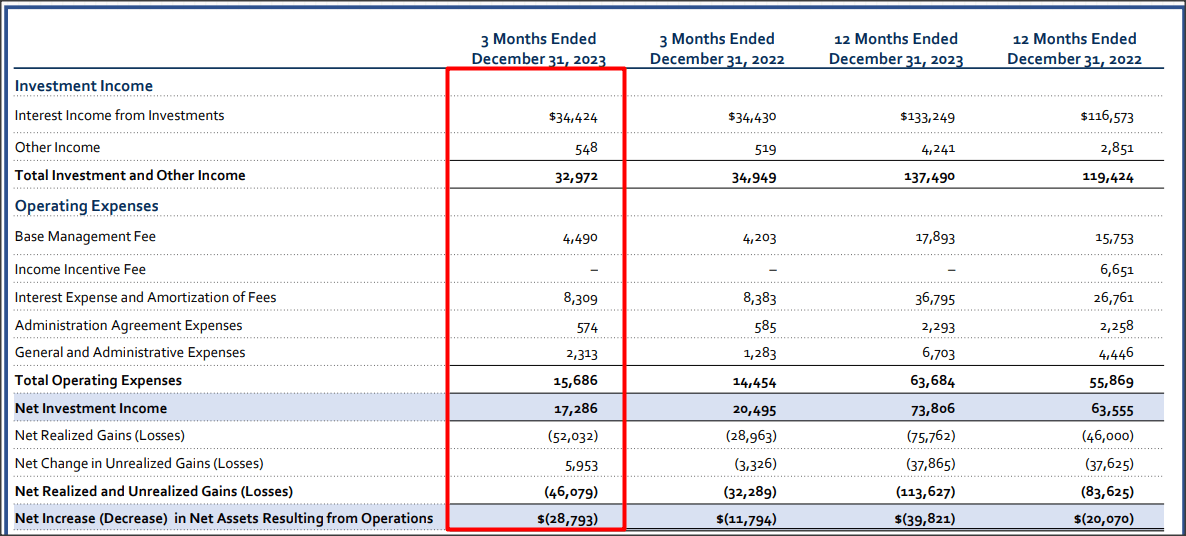

TriplePoint Enterprise Progress’s investments, based mostly on honest worth, totaled $802.1M within the fourth quarter… which mirrored a decline of seven.8% quarter over quarter. The BDC realized losses of $52.1M in This autumn ’23 in comparison with $28.8M within the year-earlier quarter. The area of interest BDC additionally owns plenty of different belongings, value a mixed $71.8M, principally fairness in funding firms and warrants.

TriplePoint Enterprise Progress

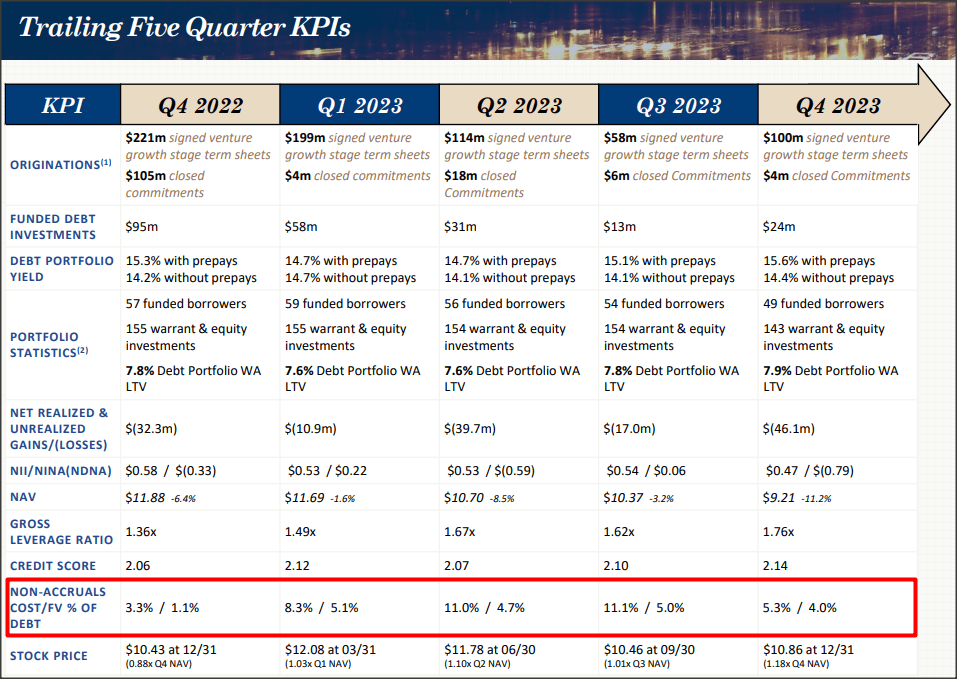

TPVG has had mortgage points up to now, which translated to increased than common non-accruals. The BDC’s non-accrual share as of December 31, 2023, was 4.0% in comparison with 5.0% within the earlier quarter. The BDC wrote off investments in 4 portfolio firms (ensuing within the $52.1M realized funding loss described above). A non-accrual share of 4.0% remains to be fairly excessive and signifies issues with the corporate’s underwriting method. Going ahead, this determine ought to be intently tracked, along with TPVG’s NII/dividend ratio.

TriplePoint Enterprise Progress

Document Full-year Internet Funding Revenue, NII Ample To Help The Dividend

TriplePoint Enterprise Progress has two particular components supporting the bull case: 1) The BDC nonetheless helps its dividend with money movement (principally from curiosity revenue), and a pair of) TPVG generates excessive funding yields.

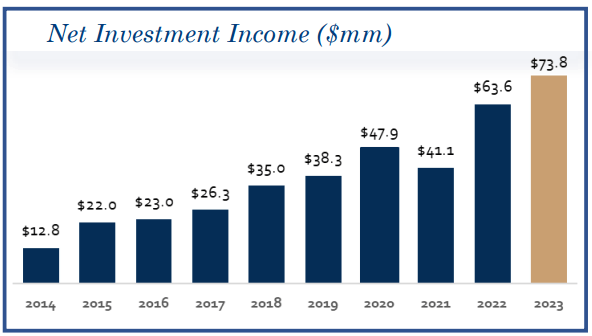

Regardless of challenges with its mortgage high quality, FY 2023 was a very good yr from a progress perspective: TriplePoint Enterprise Progress achieved its highest annual quantity of internet funding revenue, $73.8M, displaying 16% year-over-year progress.

TriplePoint Enterprise Progress

Whole This autumn ’23 curiosity revenue was $34.4M, which was primarily on the identical degree as final yr. TriplePoint Enterprise Progress’s This autumn ’23 internet funding revenue dropped 16% Y/Y to $17.3M, nonetheless, mainly because of increased common and administrative bills.

This internet funding revenue was enough to help the dividend, which presently nonetheless stands at $0.40 per share (and which was simply confirmed). Based mostly on $0.47 per share in internet funding revenue within the fourth quarter, I calculate a NII/dividend protection ratio of 118%. In FY 2023, TriplePoint Enterprise Progress generated NII of $2.07 per share, which calculates to a NII/dividend protection ratio 129%… so regardless of a slightly poor credit score profile, TPVG nonetheless manages to help its $0.40 per share quarterly dividend. A dividend lower, within the close to time period, subsequently will not be doubtless, for my part. Based mostly off of a $1.60 per-share annual distribution, TriplePoint Enterprise Progress’s shares presently yield 16.8%.

TriplePoint Enterprise Progress

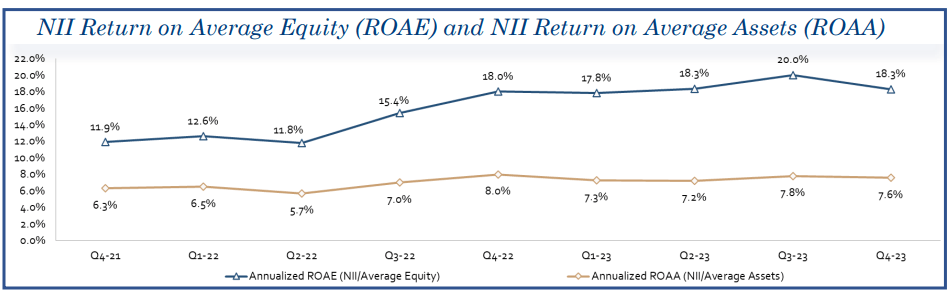

As to the second level, yields, TriplePoint Enterprise Progress is seeing favorable NII returns on its invested fairness capital. Within the fourth quarter, the BDC generated a strong 18.3% NII return on its common fairness, barely down from 20.0% in Q3 ’23, as returns have been boosted by rate of interest tailwinds. The BDC’s comparatively sturdy NII/dividend protection and double-digit NII yields are two the explanation why I preserve my maintain ranking for TPVG regardless of a major drop in NAV in This autumn ’23.

TriplePoint Enterprise Progress

TriplePoint Enterprise Progress’s Valuation

After Thursday’s drop, TriplePoint Enterprise Progress is priced at a P/NAV ratio of 1.03x, which means the BDC is buying and selling at solely a slight premium to its internet asset worth… which fell 11% to $9.21 per share on the finish of the December quarter because of funding write-offs. The BDC has traded, on common, at a P/NAV ratio of 1.09X within the final three years and the poorer-than-average mortgage high quality profile has led to a a lot decrease valuation multiplier relative to its area of interest rivals.

Hercules Capital, which is form of the gold commonplace within the venture-focused BDC area of interest, is buying and selling at a considerably increased NAV premium as a result of reality it has achieved sturdy portfolio and NII progress over time. I not too long ago down-graded HTGC to carry due to the corporate’s excessive valuation (near-60% NAV premium, considerably above 3-year common, see beneath). Horizon Expertise (HRZN), is a way more inexpensive BDC selection for buyers to need to enhance their publicity to the expertise/enterprise sector. I see Horizon Expertise as a promising yield play for dividend buyers.

Though TPVG has a a lot decrease NAV ratio than its area of interest BDC rivals, I consider the consideration of all necessary components — 11% Q/Q drop in NAV, great amount of realized losses, but in addition a supported dividend — makes the BDC nonetheless a maintain right here. My honest worth estimate is TPVG’s up to date internet asset worth of $9.21 per share. I mission that TPVG will commerce at or beneath internet asset worth for some time following the This autumn ’23 reviews, as NAV declines and funding losses hardly ever appeal to new dividend consumers.

| Title | This autumn NAV/share | Share Worth | P/NAV | Prem./Disc. NAV | 3-12 months Common Premium |

| TriplePoint Enterprise Progress | $9.21 | $9.53 | 1.03X | 3.5% | 9.1% |

| Hercules Capital | $11.43 | $18.15 | 1.59X | 58.8% | 43.9% |

| Horizon Expertise | $9.71 | $11.57 | 1.19X | 19.2% | 23.0% |

(Supply: Writer)

Dangers With TriplePoint Enterprise Progress

TriplePoint Enterprise Progress is a kind of BDCs the place you’d need to intently observe the standard/efficiency of the debt portfolio and the non-accrual share. From a NII/dividend protection perspective, the dividend seems to be well-supported, not less than in the intervening time and isn’t imminently headed for a lower, for my part. Given the comparatively excessive non-accrual share of 4.0%, nonetheless, I consider that dividend buyers would solely need to make investments a really small p.c of their obtainable assets right into a high-risk BDC like TriplePoint Enterprise Progress.

Closing Ideas

TriplePoint Enterprise Progress will not be a BDC that you could purchase and maintain eternally. It’s a must to keep alert and comply with intently what is occurring on the portfolio degree, largely due to TriplePoint Enterprise Progress’s suboptimal mortgage high quality profile. Nonetheless, the BDC did handle to help its quarterly dividend of $0.40 per share with NII and the non-accrual profile did get a bit higher Q/Q. With a FY 2023 NII/dividend ratio of 129%, I consider the dividend ought to be moderately protected within the subsequent quarters, however dangers total have elevated following the report of an 11% NAV Q/Q drop. On condition that TriplePoint Enterprise Progress additionally achieves excessive NII returns on common fairness, there’s an argument to be made for proudly owning TPVG, but it surely should not be an outsized place. Consequently, I preserve my maintain ranking after This autumn ’23 earnings.

{kind=link}