I’m bearish on Tesla (NASDAQ:TSLA), and I can’t assist however assume that Elon Musk’s announcement relating to the unveiling of a Robotaxi on August 8 is one thing of a distraction. So, why would Musk be distracting us? Properly, automobile gross sales are slowing, margins are falling, and Tesla’s dominance within the electrical automobile (EV) section is over. Plus, the inventory’s valuation is excessive. For this reason I’m bearish on TSLA inventory, however I don’t count on it to maneuver a lot till we all know what Musk has in retailer for us on August 8.

Tesla’s Efficiency Is Underwhelming

In Q1, Tesla reported a 9% decline in quarterly income — the steepest year-over-year decline since 2012 — and a 48% lower in adjusted revenue. The corporate’s adjusted earnings per share (EPS) got here in at 45 cents versus the anticipated 49 cents. Additionally, income for the quarter fell to $21.3 billion — lower than the $22.2 billion the market had anticipated.

Income fell each on a year-over-year foundation and sequentially. In the meantime, internet earnings dropped 55% to $1.13 billion from $2.51 billion a 12 months in the past. On a non-adjusted foundation, internet earnings per share fell from 73 cents a 12 months in the past to 34 cents in Q1 2024. Furthermore, in an more and more aggressive market, Tesla’s value cuts negatively impacted margins with no apparent finish in sight.

Nonetheless, Musk additionally pointed to unexpected challenges as a cause for the corporate’s underperformance. “We navigated a number of unexpected challenges in addition to the ramp of the up to date Mannequin 3 in Fremont. As all of us have seen, the EV adoption charge globally is underneath stress, and quite a lot of different order producers are pulling again on EVs and pursuing plug-in hybrids as an alternative. We imagine this isn’t the best technique, and electrical autos will in the end dominate the market,” Musk mentioned within the Q1 earnings name.

Am I Underestimating Tesla’s AI Potential?

In Q1, Tesla’s free money movement turned damaging. The Austin-based firm reported a deficit of $2.53 billion, representing a big change from a 12 months in the past when Tesla had a free money movement of $441 million. Within the fourth quarter of 2023, Tesla reported free money movement of $2.06 billion. Tesla defined that the damaging money movement was on account of a $2.7 billion improve in stock and $1 billion in capital expenditures on synthetic intelligence (AI) infrastructure.

AI is definitely the buzzword of investing at this second in time, and I don’t imagine that it’s overused. Nonetheless, some analysts are arguing that traders shouldn’t be valuing Tesla as a automotive firm however as a tech firm on the forefront of AI.

I’m slightly skeptical about this, although I respect that Tesla has AI capabilities in areas like manufacturing, the Tesla Bot, and vitality buying and selling. Thus far, although, I’m but to be satisfied that these are components of the enterprise with revenue-generating capability that’s remotely comparable with automotive manufacturing.

In fact, the AI-enabled Robotaxi might change my opinion. The query is whether or not Tesla has actually managed to realize a quantum leap in autonomous expertise. This would actually put Tesla within the driving seat and set up its dominance within the autonomous section.

The expansion of the Robotaxi section would additionally open up one other revenue-generating section, which does look extremely engaging. Autonomous vehicles require a lot of computational energy, however that energy would solely be used when the automobile is energetic. This implies these spectacular computer systems will solely be used a fraction of the time.

Much like Amazon (NASDAQ:AMZN) Net Companies, Tesla might promote this spare capability and create a brand new and probably sizeable income stream. “It looks as if sort of a no brainer to say, OK, if we’ve bought tens of millions after which tens of tens of millions of autos on the market the place the computer systems are idle more often than not that we would effectively have them do one thing helpful,” Musk mentioned within the Q1 outcomes name, including that Tesla might have 100 gigawatts of “helpful compute.”

Tesla’s Valuation and Musk’s Guarantees

Musk has a behavior of overpromising and underdelivering. So, this is the reason I stay bearish on Tesla. I’ve but to see proof that Tesla is about to drop a completely autonomous automobile, which occurs to have spare computational capability that can be utilized and bought as a part of some Tesla cloud.

This wouldn’t be an issue if Tesla’s valuation was in keeping with its friends. Nonetheless, Tesla is at present buying and selling round 70x ahead earnings. What’s extra, analysts clearly aren’t satisfied that progress will decide up within the medium time period, with a price-to-earnings-to-growth ratio of 5.75x.

For now, the promise of an autonomous automobile seems to be preserving the share value elevated regardless of the dearth of concrete info. All eyes, subsequently, are on August 8. I imagine the inventory might tread water till then.

Is Tesla Inventory a Purchase, In response to Analysts?

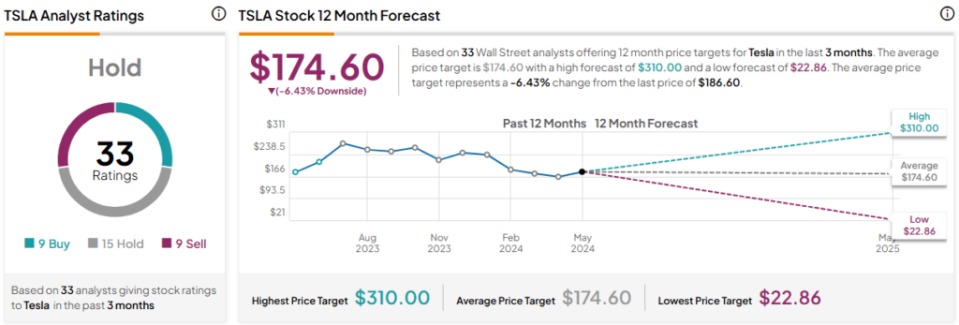

On TipRanks, Tesla is available in as a Maintain based mostly on 9 Buys, 15 Holds, and 9 Promote scores assigned by analysts previously three months. The common Tesla inventory value goal is $174.60, implying 6.4% draw back potential.

The Backside Line on Tesla Inventory

Personally, I’m skeptical as as to whether Tesla has actually made a breakthrough in autonomous autos. Nonetheless, I settle for that Robotaxi and totally autonomous autos, on the whole, have enormous potential. This potential isn’t restricted to the highway but in addition, as Musk mentioned, the power to promote unused computing energy to the remainder of the market. Nonetheless, at 70x ahead earnings, I merely can’t put my cash behind Tesla.

{kind=link}