Within the final 5 years, shares of Celsius Holdings (NASDAQ: CELH) are up 6,290%. Meaning for each $1,000 somebody invested in Celsius 5 years in the past, it’s price over $60,000 as we speak. Not dangerous. The proprietor of the Celsius power drink model has grown its income like gangbusters because it good points market share within the extremely worthwhile power drink house and makes buyers a fortune within the course of.

However what is going to the following 5 years appear to be? The corporate has some huge plans up its sleeve and simply reported one other sturdy earnings report, sending the inventory near all-time highs. Let’s have a look at the place this monster grower might find yourself in 5 years and whether or not the inventory is a purchase at as we speak’s costs.

Slowing income progress, increasing margins

On its face, income progress regarded a bit weak within the first quarter of 2024. It was simply 37% yr over yr within the interval in comparison with 102% within the fourth quarter of 2023. Gross sales hit $355.7 million — a report — however buyers must be rightfully involved about slowing gross sales progress as this enterprise matures.

Nonetheless, it appears like administration had an honest rationalization for the large slowdown: stock buildup amongst its retailers and distributors. In 2023, Celsius’s distributors had been build up stock in anticipation of demand, which led to a pull-forward in income progress and people 100%+ numbers.

Now, the other is going on, which is inflicting income progress to sluggish significantly. From a buyer standpoint, retail gross sales of Celsius had been estimated to have grown 72% yr over yr within the first quarter in america, which is nearer to the true progress charge of the Celsius model. It now has an 11.5% class share in its residence market.

A maturing enterprise means increasing revenue margins. Celsius had a report 23.4% working margin within the first quarter, which is a good signal for shareholders. It’s closing in on competitor Monster Beverage, which had an working margin of 28.5% in the identical interval.

Can the model work internationally?

There’s nonetheless room for Celsius to develop in america. With how briskly it’s gaining market share, it would not shock me if the corporate doubled or tripled income by way of market share good points and value hikes. This could assist consolidated income develop for years to come back, though you should not anticipate 100% progress eternally.

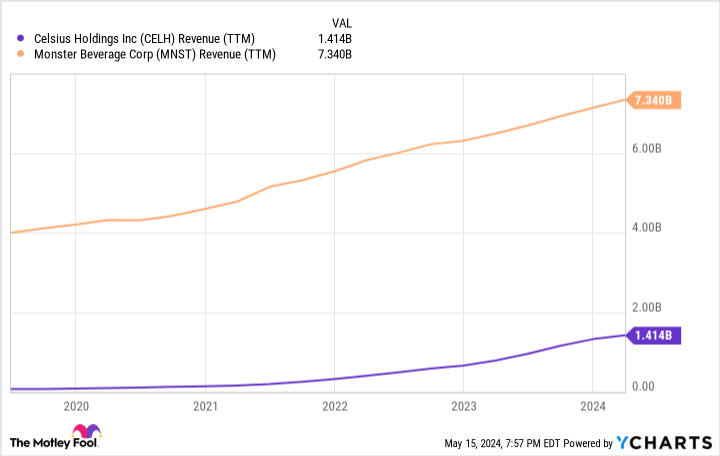

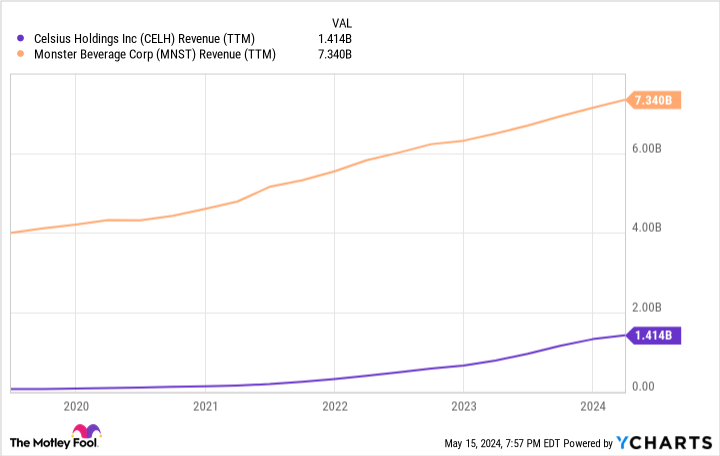

Ultimately, the corporate might want to broaden internationally if it hopes to continue to grow income and match the dimensions of the business behemoth Monster Beverage. Monster does round $7.3 billion in annual income in comparison with Celsius’s $1.4 billion. The model has introduced expansions into France, Australia, the UK, and New Zealand in current months.

To this point, this hasn’t proven up on the revenue assertion. Worldwide gross sales had been simply $16.2 million within the first quarter, or lower than 5% of general gross sales. Buyers cannot anticipate these markets to catch fireplace in a single day, however there must be some concern that Celsius is unable to duplicate the success it has had in america in different nations. Worldwide income will probably be an necessary quantity to trace over the following few years as will probably be the important thing to maintaining these excessive ranges of income progress for the model.

The place will Celsius inventory be in 5 years?

Celsius is closing in on $1.5 billion in annual gross sales. Let’s assume it retains rising market share in america, is ready to implement value will increase to maintain up with inflation, and at last sees some modest success in new nations over the following 5 years. If this occurs, I believe Celsius might 3x its income to $4.5 billion 5 years from now.

Let’s additionally assume revenue margins broaden to 25% and apply them to a $4.5 billion income base. That’s $1.125 billion in annual earnings. Immediately, Celsius has a market capitalization of $22 billion, or a price-to-earnings ratio (P/E) of 20 based mostly on this five-year earnings projection. Once more, these are projected earnings 5 years into the long run, not as we speak’s earnings. This P/E is barely decrease than the typical P/E for the inventory market as we speak.

What this tells me is that numerous sturdy income progress is already priced into Celsius inventory, even for those who anticipate income to triple over the following 5 years. Because of this, I would not be stunned to see Celsius shares at an analogous degree 5 years from now, making the inventory a dangerous guess for buyers for the time being.

Celsius is a fast-growing firm. However that does not mechanically imply the inventory is a purchase.

The place to take a position $1,000 proper now

When our analyst staff has a inventory tip, it will probably pay to pay attention. In spite of everything, the publication they’ve run for twenty years, Motley Idiot Inventory Advisor, has greater than tripled the market.*

They simply revealed what they imagine are the 10 greatest shares for buyers to purchase proper now… and Celsius made the listing — however there are 9 different shares you could be overlooking.

*Inventory Advisor returns as of Might 13, 2024

Brett Schafer has no place in any of the shares talked about. The Motley Idiot has positions in and recommends Celsius and Monster Beverage. The Motley Idiot has a disclosure coverage.

The place Will Monster Development Inventory Celsius Be In 5 Years? was initially printed by The Motley Idiot

{kind=link}